Market Estimation & Definition

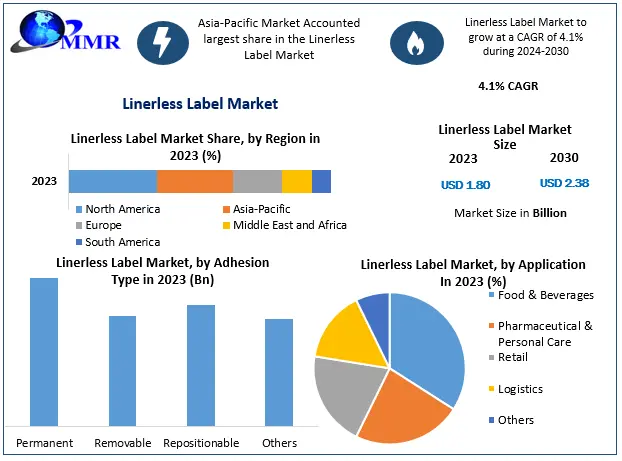

The Linerless Label Industry, valued at approximately USD 1.80 billion in 2023, is poised to surpass USD 2.38 billion by 2030, growing at a projected CAGR of 4.1%. Linerless labels are pressure-sensitive labels produced without a traditional release liner. Unlike conventional labels, these are applied directly to products or packaging without generating backing waste, making them a sustainable labeling solution for businesses prioritizing operational efficiency and environmental responsibility.

These labels offer enhanced productivity by reducing material consumption, logistics costs, and waste disposal expenses. Their versatility allows for broad application across food & beverage, logistics, retail, pharmaceuticals, and personal care industries.

Market Overview:

Linerless labels are those that do not have a backing paper and stick to the surface when pressure is applied. Its job is to keep the contents of the package safe from air, moisture, and pollution from outside sources. Linerless labels are made without a release liner, which decreases the amount of raw material used in label production and makes them an environmentally friendly option. The lack of a liner layer saves end-users money on additional labor, storage, and transportation, as well as reducing industrial waste and carbon emissions.

Ask for Sample to Know US Tariff Impacts on Linerless Label Industry @ https://www.maximizemarketresearch.com/request-sample/122602/

Drivers

The protection of natural resources, waste reduction, and energy conservation are all major factors driving the global linerless labels market forward. The escalating demand for consumer goods, combined with the flexible packaging industry, will provide the market with numerous growth opportunities soon.

Restraints:

The inability of manufacturers to produce labels in different sizes and shapes than regular parallelogram structures is a challenge affecting the growth of the market. Manufacturers are constantly seeking unique branding products, these regular shapes may not fulfill their demand for unique trademarks, thus hindering the growth of the market.

Segmentation Analysis

The linerless label market is segmented as follows:

Based on Component,

the facestock segment had the highest market share. Facestock is a self-adhesive composite material used for printing and enhancing a brand's logo. The Facestock segment holds for about 4/5th of the label by weight and it is mandatory for the production of labels.

Based on Adhesion Type,

the repositionable segment is expected to hold the largest stake during the forecast period. On other hand, the permanent segment currently accounts for the largest share in terms of volume owing to heavy demand for such linerless labels from the retail and logistics sector.

Based on Printing Technologies,

the flexographic segment is expected to dominate the linerless labels industry, in terms of both value and volume. Flexography is one of the quickest, most flexible, cost-effective, and reliable printing methods for applying simple designs and colors to a variety of packaging materials, including waxed paper containers, corrugated cardboard boxes, and tape.

Based on Printing Ink,

water-based printing ink accounted for the largest market share in the global linerless labels market. Water-based inks have a high degree of compliance with current environmental protection requirements, which explains their high consumption in the label printing industry.

Based on the Application,

the Food & Beverage segment is expected to hold the largest share in the market during the forecast period, both based on volume and value, on account of required labels to distinguish the products from the other competitors in the industry.

Explore key trends, innovations & market forecasts: https://www.maximizemarketresearch.com/market-report/linerless-label-market/122602/

Regional Insights:

Asia Pacific, where businesses have the potential to grow and acquire market share, companies in the developed world are attempting to strategically protect their market share. This is mostly due to increased industry consolidation and the presence of a large number of players in North America and Europe attempting to tap the market. The presence of a well-established retail sector in the United States is expected to help North America develop significantly.

Key Developments:

RR Donnelley & Sons Company, one of the leading manufacturers of linerless labels, added a new linerless press to its linerless label manufacturing platform in June 2021. This allowed the company to increase its linerless label output, allowing it to provide more creative linerless labels while also improving operational efficiency.

Competitive Landscape

The global linerless label market is highly competitive, with several major players actively pursuing innovation and market expansion strategies. Leading companies focus on R&D to enhance label durability, sustainability, and printing quality. Strategic mergers, acquisitions, and partnerships are common as firms aim to diversify product portfolios and broaden geographic reach.

Key players include

1. Coveris

2. Avery Dennison Corporation

3. Lexit Group AS

4. Hub Labels

5. Optimum Group

6. Bostik

7. Ravenwood Packaging

8. Innovia Films

9. Constantania Flexibles

Press Release Conclusion

The linerless label market is entering a promising growth phase driven by sustainability, operational efficiency, and technology integration. As industries increasingly prioritize waste reduction and automation, linerless labels are emerging as the preferred choice for modern, efficient, and eco-friendly labeling. The market’s upward trajectory is expected to continue, fueled by innovations in smart labeling, printing technologies, and advanced adhesives, solidifying its role as a cornerstone of the global packaging industry.

About Us