Tire Cord Fabrics Market Size, Demand Outlook, and Strategic Insights (2024-2030)

Tire Cord Fabrics Market Overview

Maximize Market Research is a Business Consultancy Firm that has published a detailed analysis of the “Tire Cord Fabrics Market”. The report includes key business insights, demand analysis, pricing analysis, and competitive landscape. The analysis in the report provides an in-depth aspect at the current status of the Tire Cord Fabrics Market, with forecasts outspreading to the year.

Gain Valuable Insights – Request Your Complimentary Sample Now @ https://www.maximizemarketresearch.com/request-sample/30320/

Tire Cord Fabrics Market Scope and Methodology:

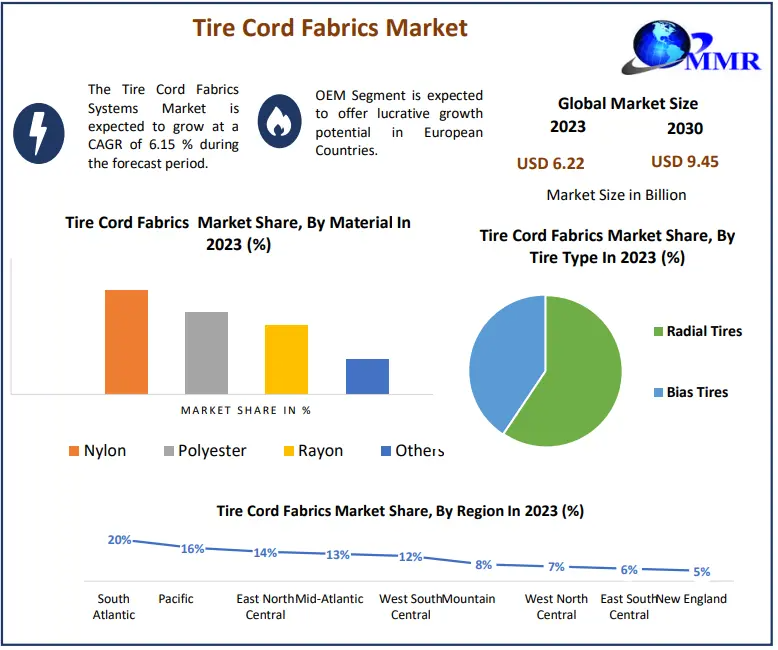

The market research report for Tire Cord Fabrics provides comprehensive information on important factors, such as those that are expected to drive the industry growth and future obstacles. This report provides stakeholders with a thorough understanding of the investment opportunities, product offerings, and competitive landscape of the Tire Cord Fabrics industry. Furthermore, it is covered in the research are the sector quantitative and qualitative aspects. Within the framework of the MMR research, regional markets for the Tire Cord Fabrics Market are evaluated in great detail.

A full description of each of the major and some of the minor components is provided by the study. Using information from primary and secondary sources, the Tire Cord Fabrics Market was created. A number of experts and academics viewpoints, official websites, scientific publications, and annual reports.

Tire Cord Fabrics Market Segmentation

by Material

Nylon

Polyester

Rayon

Others

by Tire Type

Radial Tires

Bias Tires

Feel free to request a complimentary sample copy or view a summary of the report @ https://www.maximizemarketresearch.com/request-sample/30320/

Tire Cord Fabrics Market Regional Insights

The market size, growth rate, import and export by region, and other relevant variables are all thoroughly analysed in this research. Understanding the Tire Cord Fabrics market conditions in different countries is feasible because to the researchs geographic examination. Africa, Latin America, the Middle East, Asia Pacific, and Europe put together make up the Tire Cord Fabrics market.

Tire Cord Fabrics Market Key Players

1. Hyosung Corporation - Headquarters: Seoul, South Korea

2. Kolon Industries Inc. - Headquarters: Gwacheon, South Korea

3. Kordsa Global - Headquarters: İstanbul, Turkey

4. SRF Limited - Headquarters: Gurgaon, India

5. Teijin Limited - Headquarters: Tokyo, Japan

6. Indorama Ventures Public Company Limited - Headquarters: Bangkok, Thailand

7. Century Enka Limited - Headquarters: Pune, India

Key questions answered in the Tire Cord Fabrics Market are:

What is Tire Cord Fabrics Market?

What is the growth rate of the Tire Cord Fabrics Market?

Which are the factors expected to drive the Tire Cord Fabrics Market growth?

What are the different segments of the Tire Cord Fabrics Market?

What growth strategies are the players considering to increase their presence in Tire Cord Fabrics Market?

What are the upcoming industry applications and trends for the Tire Cord Fabrics Market?

What are the recent industry trends that can be implemented to generate additional revenue streams for the Tire Cord Fabrics Market?

Who are the Tire Cord Fabricsing companies and what are their portfolios in Tire Cord Fabrics Market?

What segments are covered in the Tire Cord Fabrics Market?

Explore More Market Reports:

Global AI in Fintech Market https://www.maximizemarketresearch.com/market-report/global-ai-in-fintech-market/30669/

Global In-flight Entertainment Market https://www.maximizemarketresearch.com/market-report/global-in-flight-entertainment-market/57167/

About Maximize Market Research:

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research:

3rd Floor, Navale IT Park, Phase 2

Pune Banglore Highway, Narhe,

Pune, Maharashtra 411041, India

[email protected]

+91 96071 95908, +91 9607365656

Tire Cord Fabrics Market Overview

Maximize Market Research is a Business Consultancy Firm that has published a detailed analysis of the “Tire Cord Fabrics Market”. The report includes key business insights, demand analysis, pricing analysis, and competitive landscape. The analysis in the report provides an in-depth aspect at the current status of the Tire Cord Fabrics Market, with forecasts outspreading to the year.

Gain Valuable Insights – Request Your Complimentary Sample Now @ https://www.maximizemarketresearch.com/request-sample/30320/

Tire Cord Fabrics Market Scope and Methodology:

The market research report for Tire Cord Fabrics provides comprehensive information on important factors, such as those that are expected to drive the industry growth and future obstacles. This report provides stakeholders with a thorough understanding of the investment opportunities, product offerings, and competitive landscape of the Tire Cord Fabrics industry. Furthermore, it is covered in the research are the sector quantitative and qualitative aspects. Within the framework of the MMR research, regional markets for the Tire Cord Fabrics Market are evaluated in great detail.

A full description of each of the major and some of the minor components is provided by the study. Using information from primary and secondary sources, the Tire Cord Fabrics Market was created. A number of experts and academics viewpoints, official websites, scientific publications, and annual reports.

Tire Cord Fabrics Market Segmentation

by Material

Nylon

Polyester

Rayon

Others

by Tire Type

Radial Tires

Bias Tires

Feel free to request a complimentary sample copy or view a summary of the report @ https://www.maximizemarketresearch.com/request-sample/30320/

Tire Cord Fabrics Market Regional Insights

The market size, growth rate, import and export by region, and other relevant variables are all thoroughly analysed in this research. Understanding the Tire Cord Fabrics market conditions in different countries is feasible because to the researchs geographic examination. Africa, Latin America, the Middle East, Asia Pacific, and Europe put together make up the Tire Cord Fabrics market.

Tire Cord Fabrics Market Key Players

1. Hyosung Corporation - Headquarters: Seoul, South Korea

2. Kolon Industries Inc. - Headquarters: Gwacheon, South Korea

3. Kordsa Global - Headquarters: İstanbul, Turkey

4. SRF Limited - Headquarters: Gurgaon, India

5. Teijin Limited - Headquarters: Tokyo, Japan

6. Indorama Ventures Public Company Limited - Headquarters: Bangkok, Thailand

7. Century Enka Limited - Headquarters: Pune, India

Key questions answered in the Tire Cord Fabrics Market are:

What is Tire Cord Fabrics Market?

What is the growth rate of the Tire Cord Fabrics Market?

Which are the factors expected to drive the Tire Cord Fabrics Market growth?

What are the different segments of the Tire Cord Fabrics Market?

What growth strategies are the players considering to increase their presence in Tire Cord Fabrics Market?

What are the upcoming industry applications and trends for the Tire Cord Fabrics Market?

What are the recent industry trends that can be implemented to generate additional revenue streams for the Tire Cord Fabrics Market?

Who are the Tire Cord Fabricsing companies and what are their portfolios in Tire Cord Fabrics Market?

What segments are covered in the Tire Cord Fabrics Market?

Explore More Market Reports:

Global AI in Fintech Market https://www.maximizemarketresearch.com/market-report/global-ai-in-fintech-market/30669/

Global In-flight Entertainment Market https://www.maximizemarketresearch.com/market-report/global-in-flight-entertainment-market/57167/

About Maximize Market Research:

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research:

3rd Floor, Navale IT Park, Phase 2

Pune Banglore Highway, Narhe,

Pune, Maharashtra 411041, India

[email protected]

+91 96071 95908, +91 9607365656

Tire Cord Fabrics Market Size, Demand Outlook, and Strategic Insights (2024-2030)

Tire Cord Fabrics Market Overview

Maximize Market Research is a Business Consultancy Firm that has published a detailed analysis of the “Tire Cord Fabrics Market”. The report includes key business insights, demand analysis, pricing analysis, and competitive landscape. The analysis in the report provides an in-depth aspect at the current status of the Tire Cord Fabrics Market, with forecasts outspreading to the year.

Gain Valuable Insights – Request Your Complimentary Sample Now @ https://www.maximizemarketresearch.com/request-sample/30320/

Tire Cord Fabrics Market Scope and Methodology:

The market research report for Tire Cord Fabrics provides comprehensive information on important factors, such as those that are expected to drive the industry growth and future obstacles. This report provides stakeholders with a thorough understanding of the investment opportunities, product offerings, and competitive landscape of the Tire Cord Fabrics industry. Furthermore, it is covered in the research are the sector quantitative and qualitative aspects. Within the framework of the MMR research, regional markets for the Tire Cord Fabrics Market are evaluated in great detail.

A full description of each of the major and some of the minor components is provided by the study. Using information from primary and secondary sources, the Tire Cord Fabrics Market was created. A number of experts and academics viewpoints, official websites, scientific publications, and annual reports.

Tire Cord Fabrics Market Segmentation

by Material

Nylon

Polyester

Rayon

Others

by Tire Type

Radial Tires

Bias Tires

Feel free to request a complimentary sample copy or view a summary of the report @ https://www.maximizemarketresearch.com/request-sample/30320/

Tire Cord Fabrics Market Regional Insights

The market size, growth rate, import and export by region, and other relevant variables are all thoroughly analysed in this research. Understanding the Tire Cord Fabrics market conditions in different countries is feasible because to the researchs geographic examination. Africa, Latin America, the Middle East, Asia Pacific, and Europe put together make up the Tire Cord Fabrics market.

Tire Cord Fabrics Market Key Players

1. Hyosung Corporation - Headquarters: Seoul, South Korea

2. Kolon Industries Inc. - Headquarters: Gwacheon, South Korea

3. Kordsa Global - Headquarters: İstanbul, Turkey

4. SRF Limited - Headquarters: Gurgaon, India

5. Teijin Limited - Headquarters: Tokyo, Japan

6. Indorama Ventures Public Company Limited - Headquarters: Bangkok, Thailand

7. Century Enka Limited - Headquarters: Pune, India

Key questions answered in the Tire Cord Fabrics Market are:

What is Tire Cord Fabrics Market?

What is the growth rate of the Tire Cord Fabrics Market?

Which are the factors expected to drive the Tire Cord Fabrics Market growth?

What are the different segments of the Tire Cord Fabrics Market?

What growth strategies are the players considering to increase their presence in Tire Cord Fabrics Market?

What are the upcoming industry applications and trends for the Tire Cord Fabrics Market?

What are the recent industry trends that can be implemented to generate additional revenue streams for the Tire Cord Fabrics Market?

Who are the Tire Cord Fabricsing companies and what are their portfolios in Tire Cord Fabrics Market?

What segments are covered in the Tire Cord Fabrics Market?

Explore More Market Reports:

Global AI in Fintech Market https://www.maximizemarketresearch.com/market-report/global-ai-in-fintech-market/30669/

Global In-flight Entertainment Market https://www.maximizemarketresearch.com/market-report/global-in-flight-entertainment-market/57167/

About Maximize Market Research:

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research:

3rd Floor, Navale IT Park, Phase 2

Pune Banglore Highway, Narhe,

Pune, Maharashtra 411041, India

[email protected]

+91 96071 95908, +91 9607365656

0 Bình luận

0 Chia sẻ

613 Lượt xem