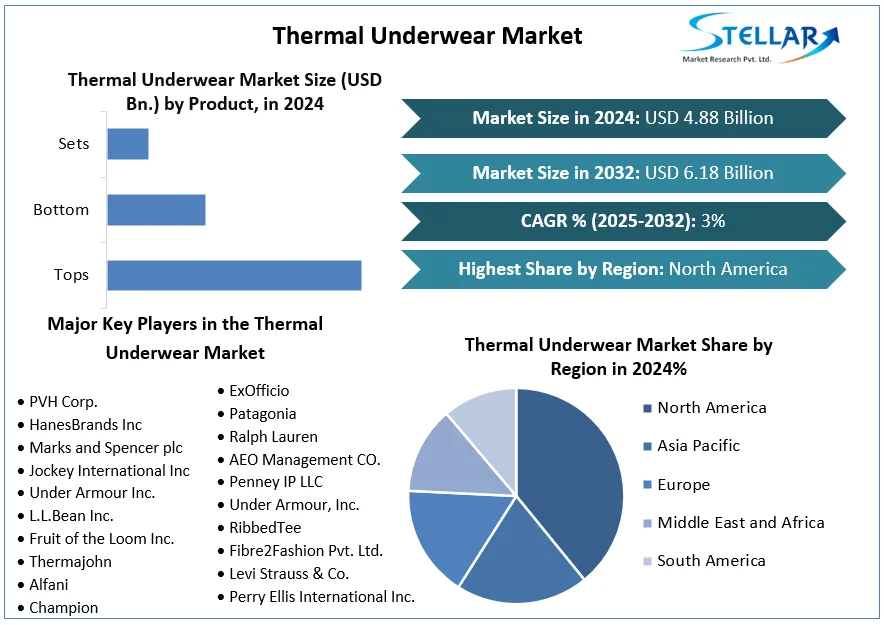

Thermal Underwear Market Size to Grow at a CAGR of 3% in the Forecast Period of 2025-2032

Thermal Underwear Market Projected to Reach USD 6.18 Billion by 2032

Market Overview

The global thermal underwear market was valued at USD 4.88 billion in 2024 and is expected to grow at a compound annual growth rate (CAGR) of 3% from 2025 to 2032, reaching approximately USD 6.18 billion by 2032.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Thermal-Underwear-Market/1904

Key Market Drivers

Cold Weather Apparel Demand: Thermal underwear serves as essential cold-weather apparel, particularly in regions with harsh winters, driving consistent demand.

Technological Advancements: Innovations in fabric materials, such as the development of high-performance synthetic fibers and blends, have enhanced the comfort and effectiveness of thermal underwear.

Outdoor Activities Participation: Increased participation in outdoor recreational activities, especially in colder climates, has contributed to the growing need for thermal underwear.

Market Segmentation

By Product Type: The market is segmented into tops, bottoms, and sets, with sets being the most popular due to their convenience and comprehensive coverage.

By Material Type: Materials commonly used include cotton, synthetic fibers, wool, and blends, with synthetic materials leading due to their durability and moisture-wicking properties.

By End-User: The market caters to men, women, and children, with men's thermal apparel expected to grow at a CAGR of 3.64%.

By Distribution Channel: Thermal underwear is sold through various channels, including online platforms and offline retail stores.

Regional Insights

North America: The largest market share is held by North America, driven by extreme weather conditions and strong retail performance.

Europe: Europe is the fastest-growing market, with increasing demand for thermal underwear due to cold climates and outdoor activities.

Competitive Landscape

Key players in the thermal underwear market include:

Calvin Klein Inc.: Known for stylish and comfortable thermal wear.

Hanes Brands Inc.: Offers a wide range of affordable thermal underwear.

Under Armour Inc.: Specializes in high-performance thermal apparel.

Smartwool LLC: Focuses on wool-based thermal wear for outdoor enthusiasts.

L.L.Bean Inc.: Provides durable and functional thermal underwear for cold-weather activities.

Conclusion

The thermal underwear market is poised for steady growth, driven by technological advancements, increased participation in outdoor activities, and the essential nature of thermal wear in cold climates. Companies that focus on innovation, quality, and effective marketing strategies are well-positioned to capitalize on the expanding market opportunities.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

Thermal Underwear Market Projected to Reach USD 6.18 Billion by 2032

Market Overview

The global thermal underwear market was valued at USD 4.88 billion in 2024 and is expected to grow at a compound annual growth rate (CAGR) of 3% from 2025 to 2032, reaching approximately USD 6.18 billion by 2032.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Thermal-Underwear-Market/1904

Key Market Drivers

Cold Weather Apparel Demand: Thermal underwear serves as essential cold-weather apparel, particularly in regions with harsh winters, driving consistent demand.

Technological Advancements: Innovations in fabric materials, such as the development of high-performance synthetic fibers and blends, have enhanced the comfort and effectiveness of thermal underwear.

Outdoor Activities Participation: Increased participation in outdoor recreational activities, especially in colder climates, has contributed to the growing need for thermal underwear.

Market Segmentation

By Product Type: The market is segmented into tops, bottoms, and sets, with sets being the most popular due to their convenience and comprehensive coverage.

By Material Type: Materials commonly used include cotton, synthetic fibers, wool, and blends, with synthetic materials leading due to their durability and moisture-wicking properties.

By End-User: The market caters to men, women, and children, with men's thermal apparel expected to grow at a CAGR of 3.64%.

By Distribution Channel: Thermal underwear is sold through various channels, including online platforms and offline retail stores.

Regional Insights

North America: The largest market share is held by North America, driven by extreme weather conditions and strong retail performance.

Europe: Europe is the fastest-growing market, with increasing demand for thermal underwear due to cold climates and outdoor activities.

Competitive Landscape

Key players in the thermal underwear market include:

Calvin Klein Inc.: Known for stylish and comfortable thermal wear.

Hanes Brands Inc.: Offers a wide range of affordable thermal underwear.

Under Armour Inc.: Specializes in high-performance thermal apparel.

Smartwool LLC: Focuses on wool-based thermal wear for outdoor enthusiasts.

L.L.Bean Inc.: Provides durable and functional thermal underwear for cold-weather activities.

Conclusion

The thermal underwear market is poised for steady growth, driven by technological advancements, increased participation in outdoor activities, and the essential nature of thermal wear in cold climates. Companies that focus on innovation, quality, and effective marketing strategies are well-positioned to capitalize on the expanding market opportunities.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

Thermal Underwear Market Size to Grow at a CAGR of 3% in the Forecast Period of 2025-2032

Thermal Underwear Market Projected to Reach USD 6.18 Billion by 2032

Market Overview

The global thermal underwear market was valued at USD 4.88 billion in 2024 and is expected to grow at a compound annual growth rate (CAGR) of 3% from 2025 to 2032, reaching approximately USD 6.18 billion by 2032.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Thermal-Underwear-Market/1904

Key Market Drivers

Cold Weather Apparel Demand: Thermal underwear serves as essential cold-weather apparel, particularly in regions with harsh winters, driving consistent demand.

Technological Advancements: Innovations in fabric materials, such as the development of high-performance synthetic fibers and blends, have enhanced the comfort and effectiveness of thermal underwear.

Outdoor Activities Participation: Increased participation in outdoor recreational activities, especially in colder climates, has contributed to the growing need for thermal underwear.

Market Segmentation

By Product Type: The market is segmented into tops, bottoms, and sets, with sets being the most popular due to their convenience and comprehensive coverage.

By Material Type: Materials commonly used include cotton, synthetic fibers, wool, and blends, with synthetic materials leading due to their durability and moisture-wicking properties.

By End-User: The market caters to men, women, and children, with men's thermal apparel expected to grow at a CAGR of 3.64%.

By Distribution Channel: Thermal underwear is sold through various channels, including online platforms and offline retail stores.

Regional Insights

North America: The largest market share is held by North America, driven by extreme weather conditions and strong retail performance.

Europe: Europe is the fastest-growing market, with increasing demand for thermal underwear due to cold climates and outdoor activities.

Competitive Landscape

Key players in the thermal underwear market include:

Calvin Klein Inc.: Known for stylish and comfortable thermal wear.

Hanes Brands Inc.: Offers a wide range of affordable thermal underwear.

Under Armour Inc.: Specializes in high-performance thermal apparel.

Smartwool LLC: Focuses on wool-based thermal wear for outdoor enthusiasts.

L.L.Bean Inc.: Provides durable and functional thermal underwear for cold-weather activities.

Conclusion

The thermal underwear market is poised for steady growth, driven by technological advancements, increased participation in outdoor activities, and the essential nature of thermal wear in cold climates. Companies that focus on innovation, quality, and effective marketing strategies are well-positioned to capitalize on the expanding market opportunities.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

0 التعليقات

0 المشاركات

96 مشاهدة