Smart Home Market Growth, Share, Size

Smart Home Market – Growth, Trends, and Strategic Outlook

Market Estimation & Definition

The global smart home market is experiencing significant growth:

Fortune Business Insights estimates the market was valued at USD 121.59 billion in 2024 and is projected to reach USD 633.20 billion by 2032, growing at a compound annual growth rate (CAGR) of 23.1% from 2025 to 2032

Data Bridge Market Research reports the market was valued at USD 183.69 billion in 2024 and is expected to reach USD 949.92 billion by 2032, at a CAGR of 22.8% during the forecast period

Grand View Research estimates the market was valued at USD 127.80 billion in 2024 and is projected to reach USD 537.27 billion by 2030, growing at a CAGR of 27.0% from 2025 to 2030

Smart home technology refers to the integration of devices and systems within a home that can be controlled remotely or automatically to enhance convenience, security, energy efficiency, and overall quality of life. These technologies encompass a wide range of applications, including lighting, heating, security, entertainment, and appliances.

Request Free Sample Report:

https://www.stellarmr.com/report/req_sample/smart-home-market/2486

Market Growth Drivers & Opportunities

Several factors are contributing to the growth of the smart home market:

Advancements in Artificial Intelligence (AI) and Internet of Things (IoT): The integration of AI and IoT technologies enables smarter automation and control of home devices, leading to enhanced user experiences and increased adoption of smart home solutions.

Rising Consumer Demand for Convenience and Energy Efficiency: Consumers are increasingly seeking solutions that offer convenience, energy savings, and improved home security, driving the demand for smart home products.

Integration of Voice Assistants: The incorporation of voice-controlled assistants, such as Amazon Alexa, Google Assistant, and Apple Siri, into smart home devices has made it easier for users to interact with their home systems, further promoting market growth.

Increased Focus on Home Security: The growing concern over home security has led to the adoption of smart security systems, including cameras, doorbells, and sensors, contributing to market expansion.

Emerging Trends Shaping the Future

The smart home market is witnessing several emerging trends:

AI-Powered Smart Displays: Companies like Google and Amazon are developing smart displays with advanced AI capabilities, enabling more interactive and intuitive user experiences in managing home automation systems

Enhanced Privacy and Security Features: With the increasing adoption of smart home devices, there is a growing emphasis on incorporating robust privacy and security features to protect user data and prevent unauthorized access.

Interoperability and Standardization: The development of universal standards and protocols, such as Matter, is facilitating greater interoperability among different smart home devices and ecosystems, allowing for seamless integration and control.

Sustainability Initiatives: Manufacturers are focusing on creating energy-efficient and environmentally friendly smart home solutions to meet the growing consumer demand for sustainable products.

Segmentation Analysis

The smart home market can be segmented based on product type, technology, application, and region:

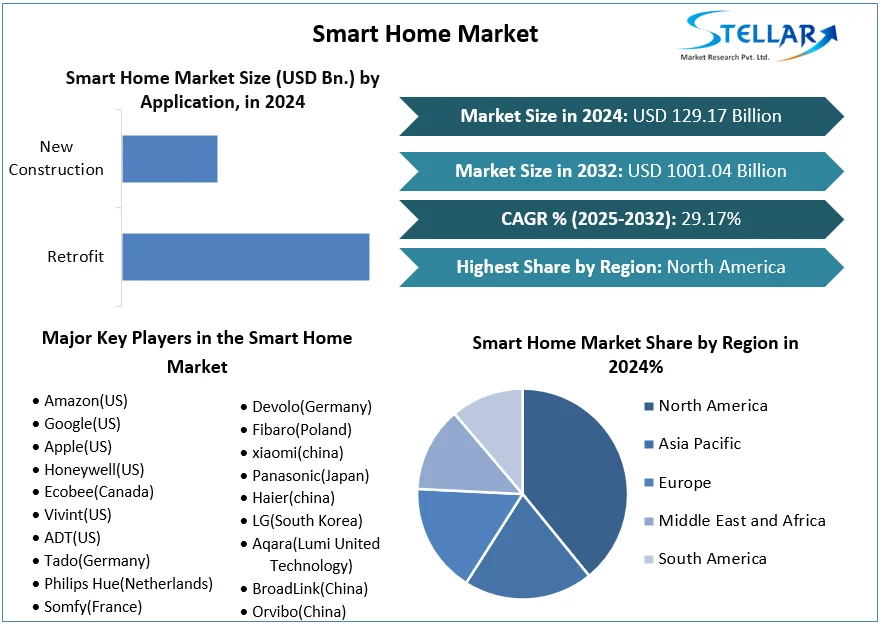

Product Type: Includes lighting control, HVAC control, security and access control, entertainment control, smart appliances, and others. Security and access control systems are expected to hold the largest market share due to increasing concerns over home safety.

Technology: Encompasses wireless and wired technologies. Wireless technologies, such as Wi-Fi, Zigbee, and Bluetooth, are widely adopted due to their ease of installation and scalability.

Application: Covers new construction and retrofit applications. The retrofit segment is anticipated to witness significant growth as homeowners seek to upgrade existing properties with smart technologies.

Region: North America currently holds the largest market share, driven by high technology adoption rates and consumer purchasing power. The Asia-Pacific region is expected to exhibit the fastest growth due to rapid urbanization and increasing disposable incomes.

Competitive Landscape

Key players in the smart home market include:

Amazon: Known for its Echo devices and Alexa voice assistant, Amazon continues to expand its smart home product offerings, including AI-powered devices and enhanced security features

Google: Offers a range of smart home products, including Nest thermostats, cameras, and speakers, and is focusing on integrating AI capabilities into its devices.

Apple: Provides smart home solutions through its HomeKit platform, enabling users to control compatible devices via iPhone, iPad, or Siri.

Samsung: Offers a variety of smart home products under its SmartThings platform, focusing on interoperability and user-friendly interfaces.

LG Electronics: Recently launched the ThinQ ON hub, supporting multiple smart home protocols and incorporating AI for autonomous home environment control .

Press Release Conclusion

The smart home market is poised for substantial growth, driven by technological advancements, increasing consumer demand for convenience and energy efficiency, and the integration of AI and IoT technologies. Companies that focus on innovation, interoperability, and user-centric solutions will be well-positioned to capitalize on the expanding global demand for smart home products.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]Smart Home Market Growth, Share, Size

Smart Home Market – Growth, Trends, and Strategic Outlook

Market Estimation & Definition

The global smart home market is experiencing significant growth:

Fortune Business Insights estimates the market was valued at USD 121.59 billion in 2024 and is projected to reach USD 633.20 billion by 2032, growing at a compound annual growth rate (CAGR) of 23.1% from 2025 to 2032

Data Bridge Market Research reports the market was valued at USD 183.69 billion in 2024 and is expected to reach USD 949.92 billion by 2032, at a CAGR of 22.8% during the forecast period

Grand View Research estimates the market was valued at USD 127.80 billion in 2024 and is projected to reach USD 537.27 billion by 2030, growing at a CAGR of 27.0% from 2025 to 2030

Smart home technology refers to the integration of devices and systems within a home that can be controlled remotely or automatically to enhance convenience, security, energy efficiency, and overall quality of life. These technologies encompass a wide range of applications, including lighting, heating, security, entertainment, and appliances.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/smart-home-market/2486

Market Growth Drivers & Opportunities

Several factors are contributing to the growth of the smart home market:

Advancements in Artificial Intelligence (AI) and Internet of Things (IoT): The integration of AI and IoT technologies enables smarter automation and control of home devices, leading to enhanced user experiences and increased adoption of smart home solutions.

Rising Consumer Demand for Convenience and Energy Efficiency: Consumers are increasingly seeking solutions that offer convenience, energy savings, and improved home security, driving the demand for smart home products.

Integration of Voice Assistants: The incorporation of voice-controlled assistants, such as Amazon Alexa, Google Assistant, and Apple Siri, into smart home devices has made it easier for users to interact with their home systems, further promoting market growth.

Increased Focus on Home Security: The growing concern over home security has led to the adoption of smart security systems, including cameras, doorbells, and sensors, contributing to market expansion.

Emerging Trends Shaping the Future

The smart home market is witnessing several emerging trends:

AI-Powered Smart Displays: Companies like Google and Amazon are developing smart displays with advanced AI capabilities, enabling more interactive and intuitive user experiences in managing home automation systems

Enhanced Privacy and Security Features: With the increasing adoption of smart home devices, there is a growing emphasis on incorporating robust privacy and security features to protect user data and prevent unauthorized access.

Interoperability and Standardization: The development of universal standards and protocols, such as Matter, is facilitating greater interoperability among different smart home devices and ecosystems, allowing for seamless integration and control.

Sustainability Initiatives: Manufacturers are focusing on creating energy-efficient and environmentally friendly smart home solutions to meet the growing consumer demand for sustainable products.

Segmentation Analysis

The smart home market can be segmented based on product type, technology, application, and region:

Product Type: Includes lighting control, HVAC control, security and access control, entertainment control, smart appliances, and others. Security and access control systems are expected to hold the largest market share due to increasing concerns over home safety.

Technology: Encompasses wireless and wired technologies. Wireless technologies, such as Wi-Fi, Zigbee, and Bluetooth, are widely adopted due to their ease of installation and scalability.

Application: Covers new construction and retrofit applications. The retrofit segment is anticipated to witness significant growth as homeowners seek to upgrade existing properties with smart technologies.

Region: North America currently holds the largest market share, driven by high technology adoption rates and consumer purchasing power. The Asia-Pacific region is expected to exhibit the fastest growth due to rapid urbanization and increasing disposable incomes.

Competitive Landscape

Key players in the smart home market include:

Amazon: Known for its Echo devices and Alexa voice assistant, Amazon continues to expand its smart home product offerings, including AI-powered devices and enhanced security features

Google: Offers a range of smart home products, including Nest thermostats, cameras, and speakers, and is focusing on integrating AI capabilities into its devices.

Apple: Provides smart home solutions through its HomeKit platform, enabling users to control compatible devices via iPhone, iPad, or Siri.

Samsung: Offers a variety of smart home products under its SmartThings platform, focusing on interoperability and user-friendly interfaces.

LG Electronics: Recently launched the ThinQ ON hub, supporting multiple smart home protocols and incorporating AI for autonomous home environment control .

Press Release Conclusion

The smart home market is poised for substantial growth, driven by technological advancements, increasing consumer demand for convenience and energy efficiency, and the integration of AI and IoT technologies. Companies that focus on innovation, interoperability, and user-centric solutions will be well-positioned to capitalize on the expanding global demand for smart home products.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]