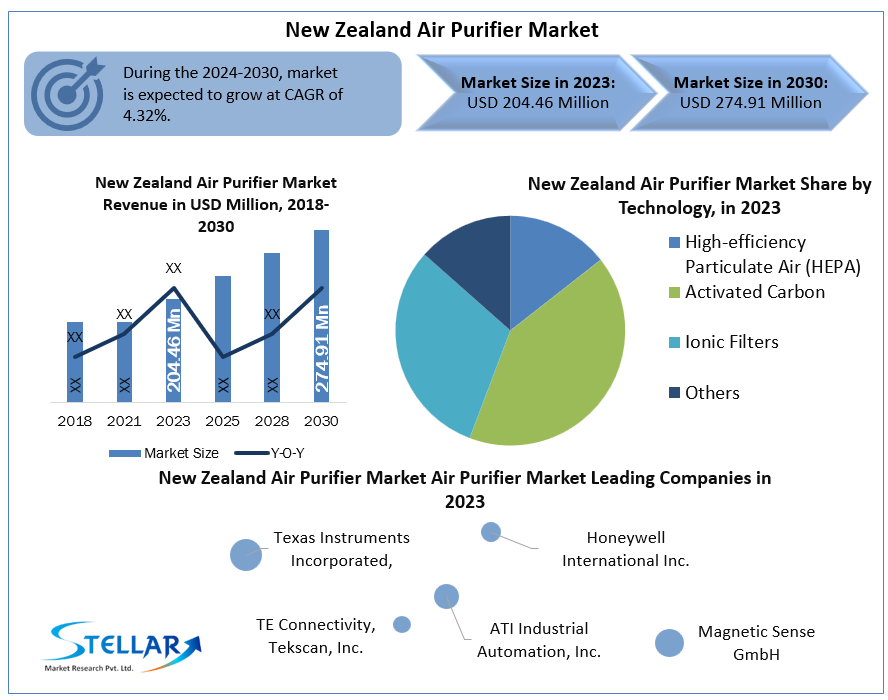

New Zealand Air Purifier Market Size To Grow At A CAGR Of 4.32% In The Forecast Period Of 2024-2030

New Zealand Air Purifier Market is poised to grow from USD 78.10 million in 2023 to USD 194.16 million by 2030, exhibiting a strong CAGR of 13.8%. Rising concerns about indoor air quality, increased awareness of respiratory health, and the proliferation of smart homes are significantly accelerating demand across residential and commercial sectors.

Request Free Sample Report:

https://www.stellarmr.com/report/req_sample/New-Zealand-Air-Purifier-Market/240

Market Estimation, Growth Drivers & Emerging Opportunities

In a nation renowned for its clean environment, the air purifier market is gaining unexpected but notable momentum. The increase in bushfire-related air pollution, allergens, and urban congestion has prompted New Zealanders to take a proactive approach to improving indoor air quality.

Key Growth Drivers:

Environmental Disruptions: Bushfire smoke from neighboring regions and seasonal pollen surges have raised public concern about air pollutants entering homes and offices.

Post-COVID Health Focus: New Zealanders are more attuned to air hygiene in both personal and shared spaces, driving air purifier purchases in schools, clinics, and residential areas.

Urbanization: Rapid urban growth in Auckland, Wellington, and Christchurch has intensified traffic-related pollution, further boosting demand.

Smart Living Trends: The adoption of smart home devices and app-connected appliances is driving interest in intelligent air purification systems.

Opportunities Ahead:

Hybrid Systems with Humidifiers/Dehumidifiers: As humidity control is crucial in New Zealand’s variable climate, devices offering dual functionalities are gaining popularity.

Eco-Friendly Models: There is a growing preference for low-energy, recyclable, and ozone-free purifiers that align with New Zealand’s sustainability values.

Subscription-Based Maintenance Models: The opportunity to offer filter replacement and maintenance subscriptions is gaining traction among tech-savvy urban households.

2024 Market Trends and Recent Developments

In 2024, the market saw a shift toward multifunctional air purifiers that integrate with other indoor climate control systems. Several local health campaigns, supported by the Ministry of Health, highlighted indoor allergens and airborne transmission risks, encouraging home and facility managers to invest in filtration systems.

Leading retailers reported a sharp increase in demand for compact, quiet, and Wi-Fi-enabled units, particularly in the wake of unusually high pollen and dust levels during spring and summer. Additionally, new entrants in the New Zealand e-commerce space introduced globally popular brands that expanded access to a wider variety of models.

Market Segmentation – Leading Segments by Market Share

By Technology:

HEPA Filtration Technology dominates the market due to its high efficiency in removing airborne particles like dust, pollen, smoke, and mold spores. It is widely used in homes and medical settings.

Activated Carbon Filters are popular for eliminating odors and volatile organic compounds (VOCs) and are often combined with HEPA in hybrid systems.

UV-Based and Ionic Air Purifiers hold a niche segment, mostly in high-traffic commercial areas and healthcare centers.

By End-Use:

Residential Segment is the market leader, accounting for the largest revenue share due to growing awareness and online product availability.

Commercial and Institutional Segment is expanding quickly, especially in schools, offices, clinics, and fitness centers where clean air is vital for occupant well-being and productivity.

Hospitality Sector is also investing in air purifiers to enhance customer satisfaction and safety, particularly in luxury accommodations and wellness retreats.

By Distribution Channel:

Retail Stores remain significant, especially for bulk purchases and personalized consultations.

Online Platforms are growing rapidly as consumers increasingly prefer the convenience of browsing, comparing, and purchasing purifiers through e-commerce websites.

Competitive Landscape – Top 5 Players and Strategic Highlights

1. Dyson (New Zealand):

Dyson leads the New Zealand market with its advanced air purifier range offering HEPA+Carbon filters and real-time air quality sensing. In 2024, it launched a new model integrating air purification with heating and cooling, suitable for New Zealand’s varied climate zones.

2. Philips Domestic Appliances:

Philips expanded its 3000i and 2000 series with ultra-quiet operation, laser particle sensors, and real-time air quality indicators. These models gained popularity in urban family homes and childcare facilities.

3. Panasonic New Zealand:

Panasonic’s “nanoe™” air purifiers continue to gain traction due to their deodorizing and virus-inhibiting technologies. In 2024, Panasonic enhanced its IoT integration features, enabling users to monitor indoor air quality remotely.

4. Xiaomi (SmartMi Division):

Xiaomi's affordable and app-compatible models, particularly the Smart Air Purifier 4 series, saw strong uptake among young professionals and apartment dwellers. Their sleek design and budget-friendly pricing gave them an edge in the online market.

5. Blueair (Unilever):

Blueair’s HealthProtect and Blue Pure ranges, emphasizing sustainability and high-grade filters, are popular in both homes and clinics. In 2024, the company focused on localized support, adding region-specific customer service and supply chain resilience.

These companies are investing in sensor-driven automation, silent operation, and low-maintenance filters to align with the evolving expectations of New Zealand consumers.

Regional Insights – Key Cities and Adoption Trends

Auckland:

As New Zealand’s most populous city, Auckland leads air purifier adoption. Increasing traffic congestion, urban sprawl, and new apartment developments are pushing consumers to invest in compact, efficient units. Local retailers and online platforms are reporting sustained growth in purifier sales post-2023.

Wellington:

The government and education sectors in Wellington have played a critical role in advancing air quality initiatives. Many offices, schools, and government buildings have integrated air purifiers as part of broader ventilation and workplace safety strategies.

Christchurch:

Christchurch faces unique challenges due to its colder climate and prolonged heating periods, which can lead to indoor air stagnation. Dual-function air purifiers with humidifying features are especially in demand.

Rural and Suburban Areas:

While penetration is lower than in urban centers, there is rising interest among homeowners affected by seasonal allergens, wood smoke, or mold issues. Energy-efficient and whisper-quiet units are particularly valued.

Conclusion & Strategic Outlook

The New Zealand Air Purifier Market is on a clear upward path, supported by increasing health consciousness, smart living trends, and a strong environmental ethos. As climate patterns change and indoor air quality becomes a vital component of public health, the demand for advanced, efficient, and sustainable purification solutions will continue to rise.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

+91 9607365656

[email protected]New Zealand Air Purifier Market Size To Grow At A CAGR Of 4.32% In The Forecast Period Of 2024-2030

New Zealand Air Purifier Market is poised to grow from USD 78.10 million in 2023 to USD 194.16 million by 2030, exhibiting a strong CAGR of 13.8%. Rising concerns about indoor air quality, increased awareness of respiratory health, and the proliferation of smart homes are significantly accelerating demand across residential and commercial sectors.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/New-Zealand-Air-Purifier-Market/240

Market Estimation, Growth Drivers & Emerging Opportunities

In a nation renowned for its clean environment, the air purifier market is gaining unexpected but notable momentum. The increase in bushfire-related air pollution, allergens, and urban congestion has prompted New Zealanders to take a proactive approach to improving indoor air quality.

Key Growth Drivers:

Environmental Disruptions: Bushfire smoke from neighboring regions and seasonal pollen surges have raised public concern about air pollutants entering homes and offices.

Post-COVID Health Focus: New Zealanders are more attuned to air hygiene in both personal and shared spaces, driving air purifier purchases in schools, clinics, and residential areas.

Urbanization: Rapid urban growth in Auckland, Wellington, and Christchurch has intensified traffic-related pollution, further boosting demand.

Smart Living Trends: The adoption of smart home devices and app-connected appliances is driving interest in intelligent air purification systems.

Opportunities Ahead:

Hybrid Systems with Humidifiers/Dehumidifiers: As humidity control is crucial in New Zealand’s variable climate, devices offering dual functionalities are gaining popularity.

Eco-Friendly Models: There is a growing preference for low-energy, recyclable, and ozone-free purifiers that align with New Zealand’s sustainability values.

Subscription-Based Maintenance Models: The opportunity to offer filter replacement and maintenance subscriptions is gaining traction among tech-savvy urban households.

2024 Market Trends and Recent Developments

In 2024, the market saw a shift toward multifunctional air purifiers that integrate with other indoor climate control systems. Several local health campaigns, supported by the Ministry of Health, highlighted indoor allergens and airborne transmission risks, encouraging home and facility managers to invest in filtration systems.

Leading retailers reported a sharp increase in demand for compact, quiet, and Wi-Fi-enabled units, particularly in the wake of unusually high pollen and dust levels during spring and summer. Additionally, new entrants in the New Zealand e-commerce space introduced globally popular brands that expanded access to a wider variety of models.

Market Segmentation – Leading Segments by Market Share

By Technology:

HEPA Filtration Technology dominates the market due to its high efficiency in removing airborne particles like dust, pollen, smoke, and mold spores. It is widely used in homes and medical settings.

Activated Carbon Filters are popular for eliminating odors and volatile organic compounds (VOCs) and are often combined with HEPA in hybrid systems.

UV-Based and Ionic Air Purifiers hold a niche segment, mostly in high-traffic commercial areas and healthcare centers.

By End-Use:

Residential Segment is the market leader, accounting for the largest revenue share due to growing awareness and online product availability.

Commercial and Institutional Segment is expanding quickly, especially in schools, offices, clinics, and fitness centers where clean air is vital for occupant well-being and productivity.

Hospitality Sector is also investing in air purifiers to enhance customer satisfaction and safety, particularly in luxury accommodations and wellness retreats.

By Distribution Channel:

Retail Stores remain significant, especially for bulk purchases and personalized consultations.

Online Platforms are growing rapidly as consumers increasingly prefer the convenience of browsing, comparing, and purchasing purifiers through e-commerce websites.

Competitive Landscape – Top 5 Players and Strategic Highlights

1. Dyson (New Zealand):

Dyson leads the New Zealand market with its advanced air purifier range offering HEPA+Carbon filters and real-time air quality sensing. In 2024, it launched a new model integrating air purification with heating and cooling, suitable for New Zealand’s varied climate zones.

2. Philips Domestic Appliances:

Philips expanded its 3000i and 2000 series with ultra-quiet operation, laser particle sensors, and real-time air quality indicators. These models gained popularity in urban family homes and childcare facilities.

3. Panasonic New Zealand:

Panasonic’s “nanoe™” air purifiers continue to gain traction due to their deodorizing and virus-inhibiting technologies. In 2024, Panasonic enhanced its IoT integration features, enabling users to monitor indoor air quality remotely.

4. Xiaomi (SmartMi Division):

Xiaomi's affordable and app-compatible models, particularly the Smart Air Purifier 4 series, saw strong uptake among young professionals and apartment dwellers. Their sleek design and budget-friendly pricing gave them an edge in the online market.

5. Blueair (Unilever):

Blueair’s HealthProtect and Blue Pure ranges, emphasizing sustainability and high-grade filters, are popular in both homes and clinics. In 2024, the company focused on localized support, adding region-specific customer service and supply chain resilience.

These companies are investing in sensor-driven automation, silent operation, and low-maintenance filters to align with the evolving expectations of New Zealand consumers.

Regional Insights – Key Cities and Adoption Trends

Auckland:

As New Zealand’s most populous city, Auckland leads air purifier adoption. Increasing traffic congestion, urban sprawl, and new apartment developments are pushing consumers to invest in compact, efficient units. Local retailers and online platforms are reporting sustained growth in purifier sales post-2023.

Wellington:

The government and education sectors in Wellington have played a critical role in advancing air quality initiatives. Many offices, schools, and government buildings have integrated air purifiers as part of broader ventilation and workplace safety strategies.

Christchurch:

Christchurch faces unique challenges due to its colder climate and prolonged heating periods, which can lead to indoor air stagnation. Dual-function air purifiers with humidifying features are especially in demand.

Rural and Suburban Areas:

While penetration is lower than in urban centers, there is rising interest among homeowners affected by seasonal allergens, wood smoke, or mold issues. Energy-efficient and whisper-quiet units are particularly valued.

Conclusion & Strategic Outlook

The New Zealand Air Purifier Market is on a clear upward path, supported by increasing health consciousness, smart living trends, and a strong environmental ethos. As climate patterns change and indoor air quality becomes a vital component of public health, the demand for advanced, efficient, and sustainable purification solutions will continue to rise.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

+91 9607365656

[email protected]