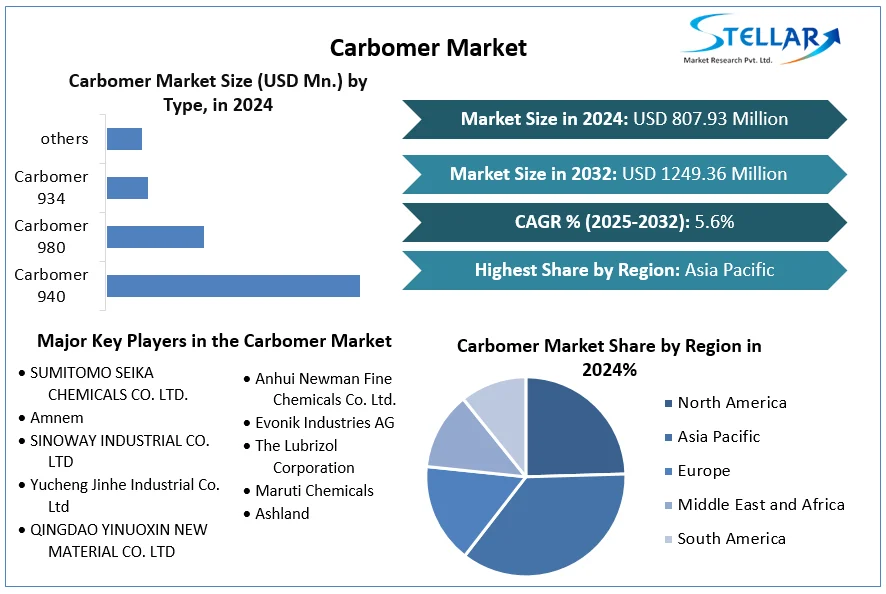

Carbomer Market Size, Share, Analysis

Global Carbomer Market – Growth, Trends, and Future Outlook (2025–2032)

Market Overview

The global carbomer market was valued at approximately USD 807.93 million in 2024 and is projected to reach USD 1,249.36 million by 2032, expanding at a Compound Annual Growth Rate (CAGR) of 5.6% during the forecast period from 2025 to 2032

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/carbomer-market/2553

Market Drivers

Several factors are contributing to the growth of the carbomer market:

Rising Demand in Personal Care and Cosmetics: Carbomers are widely used in the formulation of skincare, haircare, and cosmetic products due to their excellent thickening, emulsifying, and stabilizing properties.

Pharmaceutical Applications: In the pharmaceutical industry, carbomers are utilized as gelling agents in topical formulations and as stabilizers in oral and injectable drugs.

Growth in End-Use Industries: The increasing demand for carbomers in various end-use industries, including personal care, pharmaceuticals, and household products, is driving market growth.

Emerging Trends

The carbomer market is witnessing several emerging trends:

Sustainable Sourcing: There is a growing emphasis on sourcing raw materials for carbomer production sustainably to meet environmental and regulatory standards.

Technological Advancements: Innovations in carbomer manufacturing processes are leading to the development of more efficient and cost-effective production methods.

Customization: The demand for customized carbomer solutions tailored to specific applications is on the rise, prompting manufacturers to offer a wider range of products.

Regional Insights

Asia Pacific: Dominated the global carbomer market with a market share of 37.60% in 2023. The region's growth is attributed to rapid industrialization, urbanization, and increasing investments in water infrastructure projects

North America: Expected to witness significant growth in the carbomer market due to stringent environmental regulations and the adoption of advanced water treatment technologies.

Press Release Conclusion

The global carbomer market is poised for substantial growth, driven by increasing demand in personal care, pharmaceuticals, and other end-use industries. As industries continue to seek efficient and sustainable solutions, carbomers are expected to play a pivotal role in addressing various formulation challenges.

Recent Developments

DRDO's Indigenous Membrane for Desalination: In May 2025, the Defence Research & Development Organisation (DRDO) announced the successful development of an indigenous nanoporous multilayered polymeric membrane designed for high-pressure seawater desalination. This breakthrough enhances the country's capabilities in water purification technology, enabling efficient and sustainable desalination of seawater.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

Global Carbomer Market – Growth, Trends, and Future Outlook (2025–2032)

Market Overview

The global carbomer market was valued at approximately USD 807.93 million in 2024 and is projected to reach USD 1,249.36 million by 2032, expanding at a Compound Annual Growth Rate (CAGR) of 5.6% during the forecast period from 2025 to 2032

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/carbomer-market/2553

Market Drivers

Several factors are contributing to the growth of the carbomer market:

Rising Demand in Personal Care and Cosmetics: Carbomers are widely used in the formulation of skincare, haircare, and cosmetic products due to their excellent thickening, emulsifying, and stabilizing properties.

Pharmaceutical Applications: In the pharmaceutical industry, carbomers are utilized as gelling agents in topical formulations and as stabilizers in oral and injectable drugs.

Growth in End-Use Industries: The increasing demand for carbomers in various end-use industries, including personal care, pharmaceuticals, and household products, is driving market growth.

Emerging Trends

The carbomer market is witnessing several emerging trends:

Sustainable Sourcing: There is a growing emphasis on sourcing raw materials for carbomer production sustainably to meet environmental and regulatory standards.

Technological Advancements: Innovations in carbomer manufacturing processes are leading to the development of more efficient and cost-effective production methods.

Customization: The demand for customized carbomer solutions tailored to specific applications is on the rise, prompting manufacturers to offer a wider range of products.

Regional Insights

Asia Pacific: Dominated the global carbomer market with a market share of 37.60% in 2023. The region's growth is attributed to rapid industrialization, urbanization, and increasing investments in water infrastructure projects

North America: Expected to witness significant growth in the carbomer market due to stringent environmental regulations and the adoption of advanced water treatment technologies.

Press Release Conclusion

The global carbomer market is poised for substantial growth, driven by increasing demand in personal care, pharmaceuticals, and other end-use industries. As industries continue to seek efficient and sustainable solutions, carbomers are expected to play a pivotal role in addressing various formulation challenges.

Recent Developments

DRDO's Indigenous Membrane for Desalination: In May 2025, the Defence Research & Development Organisation (DRDO) announced the successful development of an indigenous nanoporous multilayered polymeric membrane designed for high-pressure seawater desalination. This breakthrough enhances the country's capabilities in water purification technology, enabling efficient and sustainable desalination of seawater.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

Carbomer Market Size, Share, Analysis

Global Carbomer Market – Growth, Trends, and Future Outlook (2025–2032)

Market Overview

The global carbomer market was valued at approximately USD 807.93 million in 2024 and is projected to reach USD 1,249.36 million by 2032, expanding at a Compound Annual Growth Rate (CAGR) of 5.6% during the forecast period from 2025 to 2032

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/carbomer-market/2553

Market Drivers

Several factors are contributing to the growth of the carbomer market:

Rising Demand in Personal Care and Cosmetics: Carbomers are widely used in the formulation of skincare, haircare, and cosmetic products due to their excellent thickening, emulsifying, and stabilizing properties.

Pharmaceutical Applications: In the pharmaceutical industry, carbomers are utilized as gelling agents in topical formulations and as stabilizers in oral and injectable drugs.

Growth in End-Use Industries: The increasing demand for carbomers in various end-use industries, including personal care, pharmaceuticals, and household products, is driving market growth.

Emerging Trends

The carbomer market is witnessing several emerging trends:

Sustainable Sourcing: There is a growing emphasis on sourcing raw materials for carbomer production sustainably to meet environmental and regulatory standards.

Technological Advancements: Innovations in carbomer manufacturing processes are leading to the development of more efficient and cost-effective production methods.

Customization: The demand for customized carbomer solutions tailored to specific applications is on the rise, prompting manufacturers to offer a wider range of products.

Regional Insights

Asia Pacific: Dominated the global carbomer market with a market share of 37.60% in 2023. The region's growth is attributed to rapid industrialization, urbanization, and increasing investments in water infrastructure projects

North America: Expected to witness significant growth in the carbomer market due to stringent environmental regulations and the adoption of advanced water treatment technologies.

Press Release Conclusion

The global carbomer market is poised for substantial growth, driven by increasing demand in personal care, pharmaceuticals, and other end-use industries. As industries continue to seek efficient and sustainable solutions, carbomers are expected to play a pivotal role in addressing various formulation challenges.

Recent Developments

DRDO's Indigenous Membrane for Desalination: In May 2025, the Defence Research & Development Organisation (DRDO) announced the successful development of an indigenous nanoporous multilayered polymeric membrane designed for high-pressure seawater desalination. This breakthrough enhances the country's capabilities in water purification technology, enabling efficient and sustainable desalination of seawater.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

0 Reacties

0 aandelen

942 Views