Microgreens Market Size to Grow at a CAGR of 12% in the Forecast Period of 2025-2032

Global Microgreens Market Poised for Robust Growth Through 2032

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Microgreens-Market/2027

Market Overview

The global microgreens market is experiencing significant growth, driven by increasing consumer demand for nutrient-dense foods, advancements in indoor farming technologies, and a growing awareness of the health benefits associated with microgreens. These young, edible plants are harvested at an early stage of growth and are known for their vibrant colors, intense flavors, and high concentrations of vitamins and antioxidants.

Market Size and Forecast

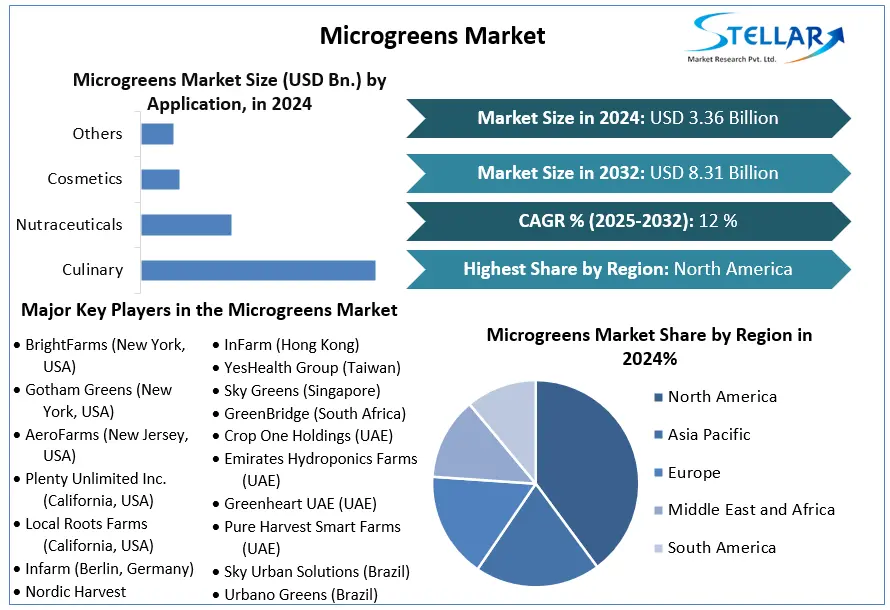

The global microgreens market was valued at approximately USD 3.24 billion in 2024 and is projected to reach USD 7.97 billion by 2032, growing at a compound annual growth rate (CAGR) of 10.5% during the forecast period from 2024 to 2032 .

Key Market Drivers

Several factors are contributing to the growth of the microgreens market:

Health Consciousness: Increasing awareness among consumers about the nutritional benefits of microgreens is driving demand. These plants are rich in vitamins, minerals, and antioxidants, making them a popular choice for health-conscious individuals.

Urban Farming Trends: The rise of urban farming and the adoption of indoor and vertical farming techniques have made it easier to cultivate microgreens in urban environments, reducing the need for large agricultural spaces.

Culinary Applications: Microgreens are increasingly used in gourmet cooking and food presentation due to their intense flavors and visual appeal, further boosting their popularity in the foodservice industry.

Regional Insights

North America: North America holds a significant share of the global microgreens market, driven by a strong demand for organic and locally sourced produce. The United States, in particular, has seen a rise in urban farming initiatives and the popularity of microgreens in culinary applications.

Europe: Europe is expected to dominate the microgreens market in 2025, with an estimated share of 40.3%. The region's well-established market ecosystem and supply chain support microgreens production and distribution .

Asia-Pacific: The Asia-Pacific region is anticipated to witness the highest growth rate during the forecast period, fueled by increasing consumer health consciousness in countries like China and India .

Market Trends

Sustainability Initiatives: There is a growing emphasis on sustainable farming practices, with many producers adopting eco-friendly methods such as hydroponics and aeroponics to cultivate microgreens.

Product Innovation: Companies are developing new varieties of microgreens and innovative packaging solutions to meet consumer preferences and extend shelf life.

Retail Expansion: Microgreens are increasingly available in supermarkets, health food stores, and online platforms, making them more accessible to a broader consumer base.

Conclusion

The global microgreens market is set for robust growth, driven by factors such as health consciousness, urban farming trends, and culinary applications. Stakeholders in the agriculture and food industries should focus on innovation, sustainability, and accessibility to capitalize on the burgeoning opportunities in this sector.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

Global Microgreens Market Poised for Robust Growth Through 2032

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Microgreens-Market/2027

Market Overview

The global microgreens market is experiencing significant growth, driven by increasing consumer demand for nutrient-dense foods, advancements in indoor farming technologies, and a growing awareness of the health benefits associated with microgreens. These young, edible plants are harvested at an early stage of growth and are known for their vibrant colors, intense flavors, and high concentrations of vitamins and antioxidants.

Market Size and Forecast

The global microgreens market was valued at approximately USD 3.24 billion in 2024 and is projected to reach USD 7.97 billion by 2032, growing at a compound annual growth rate (CAGR) of 10.5% during the forecast period from 2024 to 2032 .

Key Market Drivers

Several factors are contributing to the growth of the microgreens market:

Health Consciousness: Increasing awareness among consumers about the nutritional benefits of microgreens is driving demand. These plants are rich in vitamins, minerals, and antioxidants, making them a popular choice for health-conscious individuals.

Urban Farming Trends: The rise of urban farming and the adoption of indoor and vertical farming techniques have made it easier to cultivate microgreens in urban environments, reducing the need for large agricultural spaces.

Culinary Applications: Microgreens are increasingly used in gourmet cooking and food presentation due to their intense flavors and visual appeal, further boosting their popularity in the foodservice industry.

Regional Insights

North America: North America holds a significant share of the global microgreens market, driven by a strong demand for organic and locally sourced produce. The United States, in particular, has seen a rise in urban farming initiatives and the popularity of microgreens in culinary applications.

Europe: Europe is expected to dominate the microgreens market in 2025, with an estimated share of 40.3%. The region's well-established market ecosystem and supply chain support microgreens production and distribution .

Asia-Pacific: The Asia-Pacific region is anticipated to witness the highest growth rate during the forecast period, fueled by increasing consumer health consciousness in countries like China and India .

Market Trends

Sustainability Initiatives: There is a growing emphasis on sustainable farming practices, with many producers adopting eco-friendly methods such as hydroponics and aeroponics to cultivate microgreens.

Product Innovation: Companies are developing new varieties of microgreens and innovative packaging solutions to meet consumer preferences and extend shelf life.

Retail Expansion: Microgreens are increasingly available in supermarkets, health food stores, and online platforms, making them more accessible to a broader consumer base.

Conclusion

The global microgreens market is set for robust growth, driven by factors such as health consciousness, urban farming trends, and culinary applications. Stakeholders in the agriculture and food industries should focus on innovation, sustainability, and accessibility to capitalize on the burgeoning opportunities in this sector.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

Microgreens Market Size to Grow at a CAGR of 12% in the Forecast Period of 2025-2032

Global Microgreens Market Poised for Robust Growth Through 2032

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Microgreens-Market/2027

Market Overview

The global microgreens market is experiencing significant growth, driven by increasing consumer demand for nutrient-dense foods, advancements in indoor farming technologies, and a growing awareness of the health benefits associated with microgreens. These young, edible plants are harvested at an early stage of growth and are known for their vibrant colors, intense flavors, and high concentrations of vitamins and antioxidants.

Market Size and Forecast

The global microgreens market was valued at approximately USD 3.24 billion in 2024 and is projected to reach USD 7.97 billion by 2032, growing at a compound annual growth rate (CAGR) of 10.5% during the forecast period from 2024 to 2032 .

Key Market Drivers

Several factors are contributing to the growth of the microgreens market:

Health Consciousness: Increasing awareness among consumers about the nutritional benefits of microgreens is driving demand. These plants are rich in vitamins, minerals, and antioxidants, making them a popular choice for health-conscious individuals.

Urban Farming Trends: The rise of urban farming and the adoption of indoor and vertical farming techniques have made it easier to cultivate microgreens in urban environments, reducing the need for large agricultural spaces.

Culinary Applications: Microgreens are increasingly used in gourmet cooking and food presentation due to their intense flavors and visual appeal, further boosting their popularity in the foodservice industry.

Regional Insights

North America: North America holds a significant share of the global microgreens market, driven by a strong demand for organic and locally sourced produce. The United States, in particular, has seen a rise in urban farming initiatives and the popularity of microgreens in culinary applications.

Europe: Europe is expected to dominate the microgreens market in 2025, with an estimated share of 40.3%. The region's well-established market ecosystem and supply chain support microgreens production and distribution .

Asia-Pacific: The Asia-Pacific region is anticipated to witness the highest growth rate during the forecast period, fueled by increasing consumer health consciousness in countries like China and India .

Market Trends

Sustainability Initiatives: There is a growing emphasis on sustainable farming practices, with many producers adopting eco-friendly methods such as hydroponics and aeroponics to cultivate microgreens.

Product Innovation: Companies are developing new varieties of microgreens and innovative packaging solutions to meet consumer preferences and extend shelf life.

Retail Expansion: Microgreens are increasingly available in supermarkets, health food stores, and online platforms, making them more accessible to a broader consumer base.

Conclusion

The global microgreens market is set for robust growth, driven by factors such as health consciousness, urban farming trends, and culinary applications. Stakeholders in the agriculture and food industries should focus on innovation, sustainability, and accessibility to capitalize on the burgeoning opportunities in this sector.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

0 التعليقات

0 المشاركات

117 مشاهدة