The Railroad Tie Market Size to Grow at a CAGR of 3.7 % in the Forecast Period of 2025-2032

Railroad Tie Market Analysis and Forecast

Market Estimation & Definition

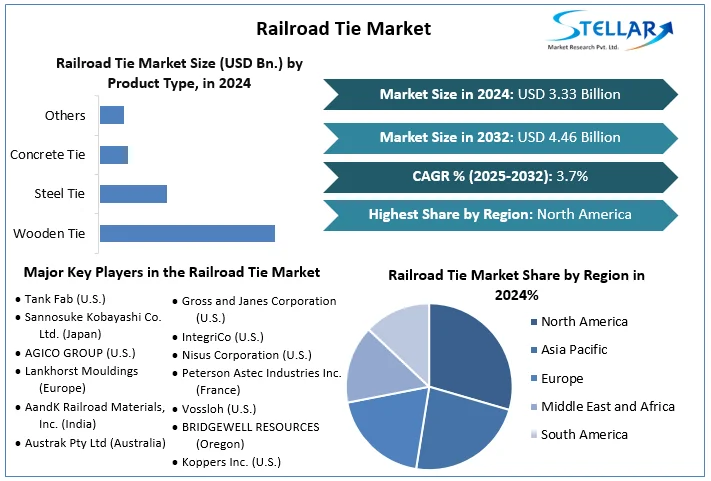

The global railroad tie market was valued at approximately USD 3.33 billion in 2024 and is projected to reach USD 8.02 billion by 2032, growing at a compound annual growth rate (CAGR) of 3.7% during the forecast period from 2025 to 2032.

Railroad ties, also known as railway sleepers, are essential components that support and secure the rails in place, ensuring the stability and alignment of the railway track. They are typically made from materials such as wood, concrete, steel, and composite materials.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Railroad-Tie-Market/853

Market Growth Drivers & Opportunities

Several factors are contributing to the growth of the railroad tie market:

Increasing Investment in Rail Infrastructure: Governments worldwide are investing heavily in the expansion and modernization of rail networks to enhance transportation efficiency and reduce carbon emissions. For instance, the U.S. Department of Transportation's Federal Railroad Administration awarded USD 8.2 billion for 10 passenger rail projects across the United States in December 2023.

Rising Demand for Concrete Ties: Concrete ties are gaining popularity due to their durability, longer lifespan, and lower maintenance costs compared to traditional wooden ties. This trend is particularly evident in regions with high-speed rail networks and heavy freight traffic.

Technological Advancements: Innovations in manufacturing processes, such as robotic assembly and automated production lines, are increasing the efficiency and uniformity of tie manufacture. This not only lowers expenses but also improves the quality and longevity of railroad ties.

Sustainability Trends: There is a growing emphasis on eco-friendly materials and practices in the railroad industry. The adoption of composite and plastic ties made from recycled materials aligns with the global shift towards sustainable and environmentally friendly solutions.

What Lies Ahead: Emerging Trends Shaping the Future

The railroad tie market is witnessing several emerging trends:

Smart Ties: Integration of sensors and smart technologies into railroad ties allows for real-time monitoring of parameters such as temperature, stress, and moisture. This data is useful for predicting maintenance, boosting operating efficiency, and improving safety.

Hybrid Plastic Ties: Hybrid plastic ties, combining recycled plastics with other materials, are gaining traction due to their durability, resistance to environmental factors, and lower maintenance requirements.

Automated Maintenance Systems: The development of automated systems for tie inspection and replacement is streamlining maintenance processes, reducing downtime, and enhancing the overall efficiency of rail operations.

Segmentation Analysis

The railroad tie market can be segmented based on type, application, and region:

By Type: Wooden ties, concrete ties, composite/plastic ties, and steel ties. Wooden ties dominate the market due to their widespread use and cost-effectiveness.

By Application: Passenger trains, freight trains, and others. Freight trains account for the largest share, driven by the increasing demand for efficient transportation of goods.

By Region: North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific holds the largest market share, owing to rapid urbanization and infrastructure development in countries like China and India.

Country-Level Analysis

United States: The U.S. railroad tie market is experiencing steady growth, primarily driven by increased demand in freight transportation and infrastructure modernization projects.

Germany: Germany's market is characterized by a strong demand for high-quality and durable ties, supported by the country's robust rail network and emphasis on sustainability.

India: India's railroad tie market is witnessing significant growth due to rapid industrialization, urbanization, and government initiatives to enhance rail infrastructure.

Competitive Analysis

Key players in the railroad tie market include:

Koppers Inc.: A leading manufacturer of treated wood products, including railroad ties, with a strong presence in North America and Europe.

Stella-Jones Inc.: A prominent producer of railway ties and other wood products, serving markets in North America and Europe.

Patriot Rail & Ports: A provider of rail transportation and logistics services, involved in the production and supply of railroad ties.

Rocla Concrete Tie, Inc.: A manufacturer of concrete ties, offering durable and low-maintenance solutions for rail infrastructure projects.

Press Release Conclusion

The railroad tie market is poised for steady growth, driven by factors such as increasing investment in rail infrastructure, rising demand for durable and sustainable materials, and technological advancements in manufacturing processes. As the market evolves, manufacturers are focusing on innovation, customization, and eco-friendly practices to meet the diverse needs of consumers. Stakeholders are encouraged to capitalize on these trends to strengthen their position in the competitive landscape.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

Railroad Tie Market Analysis and Forecast

Market Estimation & Definition

The global railroad tie market was valued at approximately USD 3.33 billion in 2024 and is projected to reach USD 8.02 billion by 2032, growing at a compound annual growth rate (CAGR) of 3.7% during the forecast period from 2025 to 2032.

Railroad ties, also known as railway sleepers, are essential components that support and secure the rails in place, ensuring the stability and alignment of the railway track. They are typically made from materials such as wood, concrete, steel, and composite materials.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Railroad-Tie-Market/853

Market Growth Drivers & Opportunities

Several factors are contributing to the growth of the railroad tie market:

Increasing Investment in Rail Infrastructure: Governments worldwide are investing heavily in the expansion and modernization of rail networks to enhance transportation efficiency and reduce carbon emissions. For instance, the U.S. Department of Transportation's Federal Railroad Administration awarded USD 8.2 billion for 10 passenger rail projects across the United States in December 2023.

Rising Demand for Concrete Ties: Concrete ties are gaining popularity due to their durability, longer lifespan, and lower maintenance costs compared to traditional wooden ties. This trend is particularly evident in regions with high-speed rail networks and heavy freight traffic.

Technological Advancements: Innovations in manufacturing processes, such as robotic assembly and automated production lines, are increasing the efficiency and uniformity of tie manufacture. This not only lowers expenses but also improves the quality and longevity of railroad ties.

Sustainability Trends: There is a growing emphasis on eco-friendly materials and practices in the railroad industry. The adoption of composite and plastic ties made from recycled materials aligns with the global shift towards sustainable and environmentally friendly solutions.

What Lies Ahead: Emerging Trends Shaping the Future

The railroad tie market is witnessing several emerging trends:

Smart Ties: Integration of sensors and smart technologies into railroad ties allows for real-time monitoring of parameters such as temperature, stress, and moisture. This data is useful for predicting maintenance, boosting operating efficiency, and improving safety.

Hybrid Plastic Ties: Hybrid plastic ties, combining recycled plastics with other materials, are gaining traction due to their durability, resistance to environmental factors, and lower maintenance requirements.

Automated Maintenance Systems: The development of automated systems for tie inspection and replacement is streamlining maintenance processes, reducing downtime, and enhancing the overall efficiency of rail operations.

Segmentation Analysis

The railroad tie market can be segmented based on type, application, and region:

By Type: Wooden ties, concrete ties, composite/plastic ties, and steel ties. Wooden ties dominate the market due to their widespread use and cost-effectiveness.

By Application: Passenger trains, freight trains, and others. Freight trains account for the largest share, driven by the increasing demand for efficient transportation of goods.

By Region: North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific holds the largest market share, owing to rapid urbanization and infrastructure development in countries like China and India.

Country-Level Analysis

United States: The U.S. railroad tie market is experiencing steady growth, primarily driven by increased demand in freight transportation and infrastructure modernization projects.

Germany: Germany's market is characterized by a strong demand for high-quality and durable ties, supported by the country's robust rail network and emphasis on sustainability.

India: India's railroad tie market is witnessing significant growth due to rapid industrialization, urbanization, and government initiatives to enhance rail infrastructure.

Competitive Analysis

Key players in the railroad tie market include:

Koppers Inc.: A leading manufacturer of treated wood products, including railroad ties, with a strong presence in North America and Europe.

Stella-Jones Inc.: A prominent producer of railway ties and other wood products, serving markets in North America and Europe.

Patriot Rail & Ports: A provider of rail transportation and logistics services, involved in the production and supply of railroad ties.

Rocla Concrete Tie, Inc.: A manufacturer of concrete ties, offering durable and low-maintenance solutions for rail infrastructure projects.

Press Release Conclusion

The railroad tie market is poised for steady growth, driven by factors such as increasing investment in rail infrastructure, rising demand for durable and sustainable materials, and technological advancements in manufacturing processes. As the market evolves, manufacturers are focusing on innovation, customization, and eco-friendly practices to meet the diverse needs of consumers. Stakeholders are encouraged to capitalize on these trends to strengthen their position in the competitive landscape.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

The Railroad Tie Market Size to Grow at a CAGR of 3.7 % in the Forecast Period of 2025-2032

Railroad Tie Market Analysis and Forecast

Market Estimation & Definition

The global railroad tie market was valued at approximately USD 3.33 billion in 2024 and is projected to reach USD 8.02 billion by 2032, growing at a compound annual growth rate (CAGR) of 3.7% during the forecast period from 2025 to 2032.

Railroad ties, also known as railway sleepers, are essential components that support and secure the rails in place, ensuring the stability and alignment of the railway track. They are typically made from materials such as wood, concrete, steel, and composite materials.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Railroad-Tie-Market/853

Market Growth Drivers & Opportunities

Several factors are contributing to the growth of the railroad tie market:

Increasing Investment in Rail Infrastructure: Governments worldwide are investing heavily in the expansion and modernization of rail networks to enhance transportation efficiency and reduce carbon emissions. For instance, the U.S. Department of Transportation's Federal Railroad Administration awarded USD 8.2 billion for 10 passenger rail projects across the United States in December 2023.

Rising Demand for Concrete Ties: Concrete ties are gaining popularity due to their durability, longer lifespan, and lower maintenance costs compared to traditional wooden ties. This trend is particularly evident in regions with high-speed rail networks and heavy freight traffic.

Technological Advancements: Innovations in manufacturing processes, such as robotic assembly and automated production lines, are increasing the efficiency and uniformity of tie manufacture. This not only lowers expenses but also improves the quality and longevity of railroad ties.

Sustainability Trends: There is a growing emphasis on eco-friendly materials and practices in the railroad industry. The adoption of composite and plastic ties made from recycled materials aligns with the global shift towards sustainable and environmentally friendly solutions.

What Lies Ahead: Emerging Trends Shaping the Future

The railroad tie market is witnessing several emerging trends:

Smart Ties: Integration of sensors and smart technologies into railroad ties allows for real-time monitoring of parameters such as temperature, stress, and moisture. This data is useful for predicting maintenance, boosting operating efficiency, and improving safety.

Hybrid Plastic Ties: Hybrid plastic ties, combining recycled plastics with other materials, are gaining traction due to their durability, resistance to environmental factors, and lower maintenance requirements.

Automated Maintenance Systems: The development of automated systems for tie inspection and replacement is streamlining maintenance processes, reducing downtime, and enhancing the overall efficiency of rail operations.

Segmentation Analysis

The railroad tie market can be segmented based on type, application, and region:

By Type: Wooden ties, concrete ties, composite/plastic ties, and steel ties. Wooden ties dominate the market due to their widespread use and cost-effectiveness.

By Application: Passenger trains, freight trains, and others. Freight trains account for the largest share, driven by the increasing demand for efficient transportation of goods.

By Region: North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific holds the largest market share, owing to rapid urbanization and infrastructure development in countries like China and India.

Country-Level Analysis

United States: The U.S. railroad tie market is experiencing steady growth, primarily driven by increased demand in freight transportation and infrastructure modernization projects.

Germany: Germany's market is characterized by a strong demand for high-quality and durable ties, supported by the country's robust rail network and emphasis on sustainability.

India: India's railroad tie market is witnessing significant growth due to rapid industrialization, urbanization, and government initiatives to enhance rail infrastructure.

Competitive Analysis

Key players in the railroad tie market include:

Koppers Inc.: A leading manufacturer of treated wood products, including railroad ties, with a strong presence in North America and Europe.

Stella-Jones Inc.: A prominent producer of railway ties and other wood products, serving markets in North America and Europe.

Patriot Rail & Ports: A provider of rail transportation and logistics services, involved in the production and supply of railroad ties.

Rocla Concrete Tie, Inc.: A manufacturer of concrete ties, offering durable and low-maintenance solutions for rail infrastructure projects.

Press Release Conclusion

The railroad tie market is poised for steady growth, driven by factors such as increasing investment in rail infrastructure, rising demand for durable and sustainable materials, and technological advancements in manufacturing processes. As the market evolves, manufacturers are focusing on innovation, customization, and eco-friendly practices to meet the diverse needs of consumers. Stakeholders are encouraged to capitalize on these trends to strengthen their position in the competitive landscape.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

0 Bình luận

0 Chia sẻ

809 Lượt xem