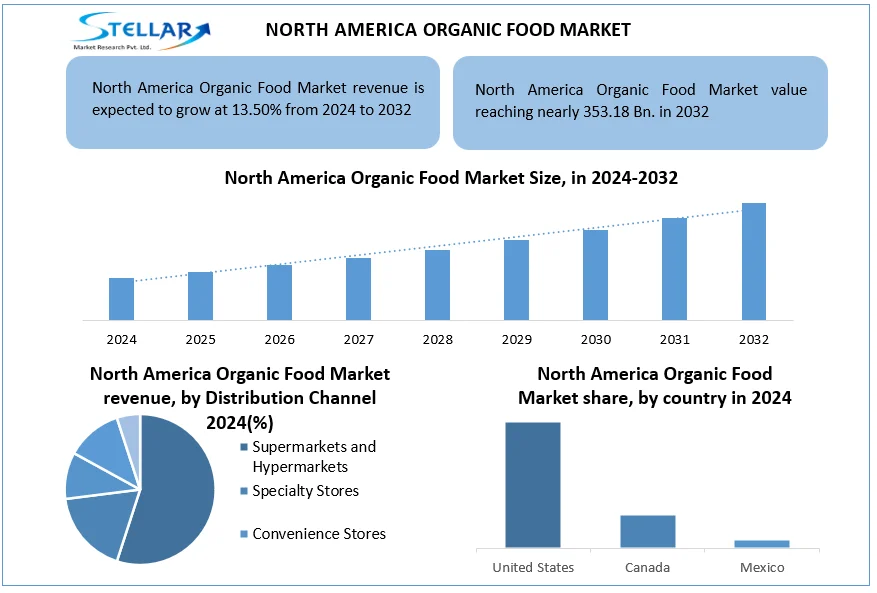

North America Organic Food Market Size to Grow at a CAGR of 13.50% in the Forecast Period of 2025-2032

North America Organic Food Market – Growth, Trends, and Strategic Outlook

Market Estimation & Definition

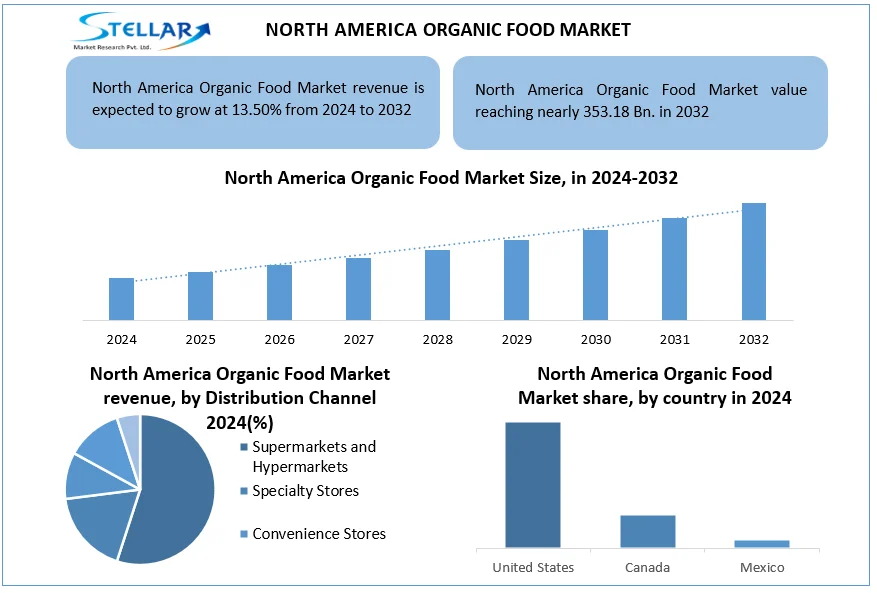

The North America organic food market is experiencing robust growth, with the U.S. market reaching USD 71.6 billion in 2024, marking a 5.2% increase from the previous year. This growth is more than double the overall food market's growth rate of 2.5% in the same period. The market's expansion is driven by increasing consumer demand for healthier, sustainable, and ethically produced food options.

Organic food refers to products grown without synthetic pesticides, fertilizers, or genetically modified organisms (GMOs), and produced following strict agricultural standards. In North America, organic certification is regulated by organizations such as the U.S. Department of Agriculture (USDA) and the Canadian Food Inspection Agency (CFIA), ensuring product integrity and consumer trust.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/north-america-organic-food-market/2721

Market Growth Drivers & Opportunities

Several factors contribute to the robust growth of the organic food market in North America:

Health Consciousness: Consumers are increasingly aware of the health risks associated with conventional farming practices, such as pesticide residues and GMOs. This awareness drives demand for organic products perceived as safer and more nutritious.

Environmental Concerns: Organic farming practices are viewed as more sustainable, with reduced environmental impact due to lower pesticide use and improved soil health. This aligns with growing consumer interest in eco-friendly products.

Government Support: Policies and subsidies supporting organic farming and certification programs enhance supply and consumer confidence in organic products.

Retail Expansion: The increasing availability of organic products in mainstream supermarkets and online platforms makes them more accessible to a broader consumer base.

What Lies Ahead: Emerging Trends Shaping the Future

The organic food market in North America is witnessing several emerging trends:

Plant-Based Alternatives: There is a growing demand for plant-based organic products, including dairy and meat substitutes, driven by health, ethical, and environmental considerations.

Clean Labeling: Consumers are seeking transparency in food labeling, favoring products with simple, recognizable ingredients and minimal processing.

Local Sourcing: Interest in locally sourced organic foods is increasing, with consumers supporting regional farmers and reducing food miles.

E-commerce Growth: Online grocery shopping for organic products is expanding, offering convenience and a wider selection to consumers.

Segmentation Analysis

The North America organic food market is segmented based on product type, distribution channel, and country:

Product Type: The market includes organic fruits and vegetables, dairy products, meat and poultry, packaged foods, and beverages. Organic fruits and vegetables hold the largest market share, driven by consumer preference for fresh, minimally processed foods.

Distribution Channel: Organic products are distributed through supermarkets and hypermarkets, specialty stores, online platforms, and direct-to-consumer channels. Supermarkets and hypermarkets are the dominant distribution channels, offering a wide range of organic products under one roof.

Country-Level Analysis:

United States: The U.S. dominates the North American organic food market, accounting for the largest share. Factors contributing to this include a high demand for organic products, advanced retail infrastructure, and supportive government policies.

Canada: Canada exhibits steady growth in the organic food market, supported by an increasing consumer base seeking healthier food options and a strong domestic organic farming sector.

Mexico: Mexico is emerging as a significant player in the organic food market, with expanding domestic production and increasing exports of organic products to North America.

Competitive Landscape

The North America organic food market is characterized by the presence of several key players:

Danone: A leading company known for its organic dairy products, Danone continues to innovate in the field of organic food.

General Mills: Offers a range of organic products, including cereals and snacks, catering to the growing demand for organic options.

Organic Valley: A cooperative of organic farmers, Organic Valley provides a wide array of organic dairy and other food products.

Whole Foods Market: A major retailer specializing in organic and natural foods, offering a comprehensive selection of organic products.

Amy’s Kitchen: Known for its organic frozen meals and snacks, Amy’s Kitchen caters to health-conscious consumers seeking convenient organic options.

Press Release Conclusion

The North America organic food market is poised for continued growth, driven by increasing consumer demand for healthier, sustainable, and ethically produced food options. With supportive government policies, expanding retail channels, and a focus on innovation, the market offers significant opportunities for stakeholders across the value chain. Companies that embrace consumer trends, invest in product development, and enhance supply chain capabilities will be well-positioned to succeed in this dynamic market.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

North America Organic Food Market – Growth, Trends, and Strategic Outlook

Market Estimation & Definition

The North America organic food market is experiencing robust growth, with the U.S. market reaching USD 71.6 billion in 2024, marking a 5.2% increase from the previous year. This growth is more than double the overall food market's growth rate of 2.5% in the same period. The market's expansion is driven by increasing consumer demand for healthier, sustainable, and ethically produced food options.

Organic food refers to products grown without synthetic pesticides, fertilizers, or genetically modified organisms (GMOs), and produced following strict agricultural standards. In North America, organic certification is regulated by organizations such as the U.S. Department of Agriculture (USDA) and the Canadian Food Inspection Agency (CFIA), ensuring product integrity and consumer trust.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/north-america-organic-food-market/2721

Market Growth Drivers & Opportunities

Several factors contribute to the robust growth of the organic food market in North America:

Health Consciousness: Consumers are increasingly aware of the health risks associated with conventional farming practices, such as pesticide residues and GMOs. This awareness drives demand for organic products perceived as safer and more nutritious.

Environmental Concerns: Organic farming practices are viewed as more sustainable, with reduced environmental impact due to lower pesticide use and improved soil health. This aligns with growing consumer interest in eco-friendly products.

Government Support: Policies and subsidies supporting organic farming and certification programs enhance supply and consumer confidence in organic products.

Retail Expansion: The increasing availability of organic products in mainstream supermarkets and online platforms makes them more accessible to a broader consumer base.

What Lies Ahead: Emerging Trends Shaping the Future

The organic food market in North America is witnessing several emerging trends:

Plant-Based Alternatives: There is a growing demand for plant-based organic products, including dairy and meat substitutes, driven by health, ethical, and environmental considerations.

Clean Labeling: Consumers are seeking transparency in food labeling, favoring products with simple, recognizable ingredients and minimal processing.

Local Sourcing: Interest in locally sourced organic foods is increasing, with consumers supporting regional farmers and reducing food miles.

E-commerce Growth: Online grocery shopping for organic products is expanding, offering convenience and a wider selection to consumers.

Segmentation Analysis

The North America organic food market is segmented based on product type, distribution channel, and country:

Product Type: The market includes organic fruits and vegetables, dairy products, meat and poultry, packaged foods, and beverages. Organic fruits and vegetables hold the largest market share, driven by consumer preference for fresh, minimally processed foods.

Distribution Channel: Organic products are distributed through supermarkets and hypermarkets, specialty stores, online platforms, and direct-to-consumer channels. Supermarkets and hypermarkets are the dominant distribution channels, offering a wide range of organic products under one roof.

Country-Level Analysis:

United States: The U.S. dominates the North American organic food market, accounting for the largest share. Factors contributing to this include a high demand for organic products, advanced retail infrastructure, and supportive government policies.

Canada: Canada exhibits steady growth in the organic food market, supported by an increasing consumer base seeking healthier food options and a strong domestic organic farming sector.

Mexico: Mexico is emerging as a significant player in the organic food market, with expanding domestic production and increasing exports of organic products to North America.

Competitive Landscape

The North America organic food market is characterized by the presence of several key players:

Danone: A leading company known for its organic dairy products, Danone continues to innovate in the field of organic food.

General Mills: Offers a range of organic products, including cereals and snacks, catering to the growing demand for organic options.

Organic Valley: A cooperative of organic farmers, Organic Valley provides a wide array of organic dairy and other food products.

Whole Foods Market: A major retailer specializing in organic and natural foods, offering a comprehensive selection of organic products.

Amy’s Kitchen: Known for its organic frozen meals and snacks, Amy’s Kitchen caters to health-conscious consumers seeking convenient organic options.

Press Release Conclusion

The North America organic food market is poised for continued growth, driven by increasing consumer demand for healthier, sustainable, and ethically produced food options. With supportive government policies, expanding retail channels, and a focus on innovation, the market offers significant opportunities for stakeholders across the value chain. Companies that embrace consumer trends, invest in product development, and enhance supply chain capabilities will be well-positioned to succeed in this dynamic market.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

North America Organic Food Market Size to Grow at a CAGR of 13.50% in the Forecast Period of 2025-2032

North America Organic Food Market – Growth, Trends, and Strategic Outlook

Market Estimation & Definition

The North America organic food market is experiencing robust growth, with the U.S. market reaching USD 71.6 billion in 2024, marking a 5.2% increase from the previous year. This growth is more than double the overall food market's growth rate of 2.5% in the same period. The market's expansion is driven by increasing consumer demand for healthier, sustainable, and ethically produced food options.

Organic food refers to products grown without synthetic pesticides, fertilizers, or genetically modified organisms (GMOs), and produced following strict agricultural standards. In North America, organic certification is regulated by organizations such as the U.S. Department of Agriculture (USDA) and the Canadian Food Inspection Agency (CFIA), ensuring product integrity and consumer trust.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/north-america-organic-food-market/2721

Market Growth Drivers & Opportunities

Several factors contribute to the robust growth of the organic food market in North America:

Health Consciousness: Consumers are increasingly aware of the health risks associated with conventional farming practices, such as pesticide residues and GMOs. This awareness drives demand for organic products perceived as safer and more nutritious.

Environmental Concerns: Organic farming practices are viewed as more sustainable, with reduced environmental impact due to lower pesticide use and improved soil health. This aligns with growing consumer interest in eco-friendly products.

Government Support: Policies and subsidies supporting organic farming and certification programs enhance supply and consumer confidence in organic products.

Retail Expansion: The increasing availability of organic products in mainstream supermarkets and online platforms makes them more accessible to a broader consumer base.

What Lies Ahead: Emerging Trends Shaping the Future

The organic food market in North America is witnessing several emerging trends:

Plant-Based Alternatives: There is a growing demand for plant-based organic products, including dairy and meat substitutes, driven by health, ethical, and environmental considerations.

Clean Labeling: Consumers are seeking transparency in food labeling, favoring products with simple, recognizable ingredients and minimal processing.

Local Sourcing: Interest in locally sourced organic foods is increasing, with consumers supporting regional farmers and reducing food miles.

E-commerce Growth: Online grocery shopping for organic products is expanding, offering convenience and a wider selection to consumers.

Segmentation Analysis

The North America organic food market is segmented based on product type, distribution channel, and country:

Product Type: The market includes organic fruits and vegetables, dairy products, meat and poultry, packaged foods, and beverages. Organic fruits and vegetables hold the largest market share, driven by consumer preference for fresh, minimally processed foods.

Distribution Channel: Organic products are distributed through supermarkets and hypermarkets, specialty stores, online platforms, and direct-to-consumer channels. Supermarkets and hypermarkets are the dominant distribution channels, offering a wide range of organic products under one roof.

Country-Level Analysis:

United States: The U.S. dominates the North American organic food market, accounting for the largest share. Factors contributing to this include a high demand for organic products, advanced retail infrastructure, and supportive government policies.

Canada: Canada exhibits steady growth in the organic food market, supported by an increasing consumer base seeking healthier food options and a strong domestic organic farming sector.

Mexico: Mexico is emerging as a significant player in the organic food market, with expanding domestic production and increasing exports of organic products to North America.

Competitive Landscape

The North America organic food market is characterized by the presence of several key players:

Danone: A leading company known for its organic dairy products, Danone continues to innovate in the field of organic food.

General Mills: Offers a range of organic products, including cereals and snacks, catering to the growing demand for organic options.

Organic Valley: A cooperative of organic farmers, Organic Valley provides a wide array of organic dairy and other food products.

Whole Foods Market: A major retailer specializing in organic and natural foods, offering a comprehensive selection of organic products.

Amy’s Kitchen: Known for its organic frozen meals and snacks, Amy’s Kitchen caters to health-conscious consumers seeking convenient organic options.

Press Release Conclusion

The North America organic food market is poised for continued growth, driven by increasing consumer demand for healthier, sustainable, and ethically produced food options. With supportive government policies, expanding retail channels, and a focus on innovation, the market offers significant opportunities for stakeholders across the value chain. Companies that embrace consumer trends, invest in product development, and enhance supply chain capabilities will be well-positioned to succeed in this dynamic market.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

0 Комментарии

0 Поделились

966 Просмотры