Data Center Chip Market to be Driven by increasing population in the Forecast Period of 2025-2032

Data Center Chip Market to Reach USD 18.79 Billion by 2030, Driven by Rising AI Workloads, Cloud Expansion, and Green Data Center Initiatives

Market Estimation, Growth Drivers & Opportunities

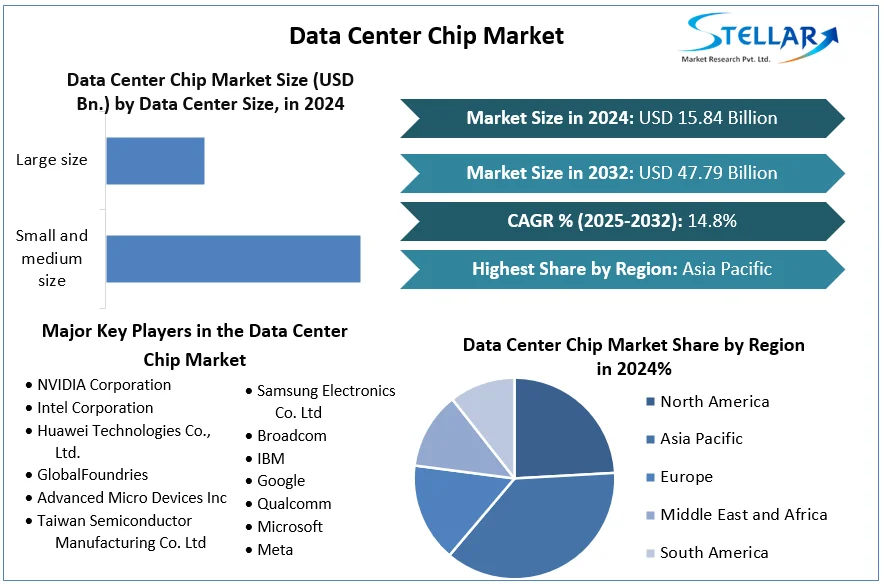

According to Stellar Market Research, the Data Center Chip Market was valued at USD 10.84 billion in 2023 and is projected to grow at a CAGR of 8.1%, reaching USD 18.79 billion by 2030. The market's upward trajectory is fueled by the explosive rise in AI-driven applications, cloud computing, and the increasing demand for hyperscale data centers.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Data-Center-Chip-Market/2282

Key Growth Drivers:

AI & Machine Learning Expansion: Massive AI workloads in language models, computer vision, and predictive analytics are prompting demand for high-performance chips with superior throughput and power efficiency.

Cloud Service Growth: Public cloud giants such as AWS, Microsoft Azure, and Google Cloud continue expanding their infrastructure, relying on powerful data center chips to ensure scalable and efficient performance.

Edge Computing: The proliferation of edge devices necessitates data processing closer to the source, driving demand for specialized chips like ASICs and FPGAs with low latency.

Sustainability Focus: The shift towards green and energy-efficient data centers is pushing innovation in low-power chips that reduce the environmental footprint of computing.

Opportunities:

Chip customization for AI/ML workloads (AI accelerators).

Development of energy-efficient chips to comply with global carbon neutrality goals.

Growing demand for quantum computing processors and neuromorphic chips.

Partnerships between chipmakers and hyperscale providers for co-designed silicon.

U.S. Market Trends and Investment in 2024

In 2024, the U.S. data center chip market saw significant investment as AI exploded across industries. Intel and AMD intensified competition by launching next-gen chips optimized for generative AI. Google’s announcement of TPU v5 and NVIDIA’s unveiling of the Blackwell GPU architecture further raised the performance bar in U.S.-based hyperscale centers.

Additionally, the CHIPS and Science Act continued to incentivize local semiconductor manufacturing. Intel expanded its Ohio facility to support domestic demand for high-performance chips. These investments aim to reduce dependence on foreign chipmakers while positioning the U.S. as a leader in AI-ready data center infrastructure.

Market Segmentation: Leading Segment by Market Share

Based on the Stellar Market Research report, the GPU (Graphics Processing Unit) segment holds the largest share of the market. GPUs have become the cornerstone of modern data centers due to their unmatched parallel processing power, critical for accelerating AI and ML workloads, deep learning, and real-time analytics.

NVIDIA dominates this segment with its H100 and new B100 Blackwell chips, which are used extensively in training large language models and powering inference at scale. Their role in delivering maximum performance-per-watt has made GPUs the preferred choice in modern AI data centers.

Competitive Analysis: Top 5 Companies

NVIDIA Corporation

The market leader in GPU-based data center chips, NVIDIA continues to lead innovation with the Hopper and Blackwell architectures. In 2024, NVIDIA deepened its partnerships with Microsoft, Meta, and Oracle to supply AI chips, expanding its dominance in hyperscale environments.

Advanced Micro Devices (AMD)

AMD gained substantial ground with its MI300 series AI accelerators, offering performance parity with NVIDIA in specific workloads. The company also expanded its EPYC server CPU lineup, focusing on power efficiency and performance-per-dollar optimization.

Intel Corporation

Intel remained strong in the CPU segment with its Xeon Scalable processors, and is increasingly investing in Gaudi AI accelerators after acquiring Habana Labs. Intel’s $20 billion Ohio fab investment in 2024 reaffirmed its commitment to secure domestic chip supply for U.S.-based data centers.

Broadcom Inc.

Broadcom provides custom ASICs and network chips used in major cloud providers’ infrastructures. In 2024, the company introduced advanced Ethernet switching chips for AI data center fabrics, enabling faster, more energy-efficient interconnects between GPUs.

Marvell Technology Group

Marvell continued to grow in the DPUs (Data Processing Units) and custom silicon segments. Its 2024 innovations in AI-specific DPUs help offload non-compute tasks from CPUs and GPUs, improving overall system efficiency and throughput.

Regional Analysis

USA: The U.S. holds a dominant share of the global data center chip market, driven by leading cloud service providers, high AI adoption, and government initiatives such as the CHIPS Act. Continued innovation and fab expansion position the country for sustained leadership.

UK: While smaller in chip manufacturing, the UK is expanding data center capacity through investments in green computing. London-based facilities now demand energy-efficient chips, pushing interest in ARM-based processors and next-gen GPUs.

Germany: Germany supports semiconductor and data center development through the EU Chips Act. Companies like SAP and Deutsche Telekom have committed to expanding local cloud operations, increasing demand for data center chips that balance performance and sustainability.

France: France is promoting sovereign cloud infrastructure and digital independence. Public and private partnerships with cloud and chip firms have led to initiatives focused on AI research centers and edge data centers, increasing demand for specialized chips.

Japan: Japan’s government announced over $7 billion in funding for semiconductor R&D in 2024. Domestic companies like Renesas and Fujitsu are collaborating with global partners to produce chips optimized for compact data centers and AI systems.

China: Despite export restrictions, China is rapidly developing homegrown data center chips. Companies like Alibaba and Huawei’s HiSilicon are investing in AI-centric processors, though geopolitical pressures challenge global expansion.

Conclusion

The Data Center Chip Market is undergoing a transformative shift, fueled by unprecedented demand for high-performance computing, cloud scalability, and AI acceleration. With the rise of generative AI, real-time analytics, and green data centers, chipmakers are racing to deliver energy-efficient, specialized silicon that meets modern computational needs.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

+91 9607365656

[email protected]

Data Center Chip Market to Reach USD 18.79 Billion by 2030, Driven by Rising AI Workloads, Cloud Expansion, and Green Data Center Initiatives

Market Estimation, Growth Drivers & Opportunities

According to Stellar Market Research, the Data Center Chip Market was valued at USD 10.84 billion in 2023 and is projected to grow at a CAGR of 8.1%, reaching USD 18.79 billion by 2030. The market's upward trajectory is fueled by the explosive rise in AI-driven applications, cloud computing, and the increasing demand for hyperscale data centers.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Data-Center-Chip-Market/2282

Key Growth Drivers:

AI & Machine Learning Expansion: Massive AI workloads in language models, computer vision, and predictive analytics are prompting demand for high-performance chips with superior throughput and power efficiency.

Cloud Service Growth: Public cloud giants such as AWS, Microsoft Azure, and Google Cloud continue expanding their infrastructure, relying on powerful data center chips to ensure scalable and efficient performance.

Edge Computing: The proliferation of edge devices necessitates data processing closer to the source, driving demand for specialized chips like ASICs and FPGAs with low latency.

Sustainability Focus: The shift towards green and energy-efficient data centers is pushing innovation in low-power chips that reduce the environmental footprint of computing.

Opportunities:

Chip customization for AI/ML workloads (AI accelerators).

Development of energy-efficient chips to comply with global carbon neutrality goals.

Growing demand for quantum computing processors and neuromorphic chips.

Partnerships between chipmakers and hyperscale providers for co-designed silicon.

U.S. Market Trends and Investment in 2024

In 2024, the U.S. data center chip market saw significant investment as AI exploded across industries. Intel and AMD intensified competition by launching next-gen chips optimized for generative AI. Google’s announcement of TPU v5 and NVIDIA’s unveiling of the Blackwell GPU architecture further raised the performance bar in U.S.-based hyperscale centers.

Additionally, the CHIPS and Science Act continued to incentivize local semiconductor manufacturing. Intel expanded its Ohio facility to support domestic demand for high-performance chips. These investments aim to reduce dependence on foreign chipmakers while positioning the U.S. as a leader in AI-ready data center infrastructure.

Market Segmentation: Leading Segment by Market Share

Based on the Stellar Market Research report, the GPU (Graphics Processing Unit) segment holds the largest share of the market. GPUs have become the cornerstone of modern data centers due to their unmatched parallel processing power, critical for accelerating AI and ML workloads, deep learning, and real-time analytics.

NVIDIA dominates this segment with its H100 and new B100 Blackwell chips, which are used extensively in training large language models and powering inference at scale. Their role in delivering maximum performance-per-watt has made GPUs the preferred choice in modern AI data centers.

Competitive Analysis: Top 5 Companies

NVIDIA Corporation

The market leader in GPU-based data center chips, NVIDIA continues to lead innovation with the Hopper and Blackwell architectures. In 2024, NVIDIA deepened its partnerships with Microsoft, Meta, and Oracle to supply AI chips, expanding its dominance in hyperscale environments.

Advanced Micro Devices (AMD)

AMD gained substantial ground with its MI300 series AI accelerators, offering performance parity with NVIDIA in specific workloads. The company also expanded its EPYC server CPU lineup, focusing on power efficiency and performance-per-dollar optimization.

Intel Corporation

Intel remained strong in the CPU segment with its Xeon Scalable processors, and is increasingly investing in Gaudi AI accelerators after acquiring Habana Labs. Intel’s $20 billion Ohio fab investment in 2024 reaffirmed its commitment to secure domestic chip supply for U.S.-based data centers.

Broadcom Inc.

Broadcom provides custom ASICs and network chips used in major cloud providers’ infrastructures. In 2024, the company introduced advanced Ethernet switching chips for AI data center fabrics, enabling faster, more energy-efficient interconnects between GPUs.

Marvell Technology Group

Marvell continued to grow in the DPUs (Data Processing Units) and custom silicon segments. Its 2024 innovations in AI-specific DPUs help offload non-compute tasks from CPUs and GPUs, improving overall system efficiency and throughput.

Regional Analysis

USA: The U.S. holds a dominant share of the global data center chip market, driven by leading cloud service providers, high AI adoption, and government initiatives such as the CHIPS Act. Continued innovation and fab expansion position the country for sustained leadership.

UK: While smaller in chip manufacturing, the UK is expanding data center capacity through investments in green computing. London-based facilities now demand energy-efficient chips, pushing interest in ARM-based processors and next-gen GPUs.

Germany: Germany supports semiconductor and data center development through the EU Chips Act. Companies like SAP and Deutsche Telekom have committed to expanding local cloud operations, increasing demand for data center chips that balance performance and sustainability.

France: France is promoting sovereign cloud infrastructure and digital independence. Public and private partnerships with cloud and chip firms have led to initiatives focused on AI research centers and edge data centers, increasing demand for specialized chips.

Japan: Japan’s government announced over $7 billion in funding for semiconductor R&D in 2024. Domestic companies like Renesas and Fujitsu are collaborating with global partners to produce chips optimized for compact data centers and AI systems.

China: Despite export restrictions, China is rapidly developing homegrown data center chips. Companies like Alibaba and Huawei’s HiSilicon are investing in AI-centric processors, though geopolitical pressures challenge global expansion.

Conclusion

The Data Center Chip Market is undergoing a transformative shift, fueled by unprecedented demand for high-performance computing, cloud scalability, and AI acceleration. With the rise of generative AI, real-time analytics, and green data centers, chipmakers are racing to deliver energy-efficient, specialized silicon that meets modern computational needs.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

+91 9607365656

[email protected]

Data Center Chip Market to be Driven by increasing population in the Forecast Period of 2025-2032

Data Center Chip Market to Reach USD 18.79 Billion by 2030, Driven by Rising AI Workloads, Cloud Expansion, and Green Data Center Initiatives

Market Estimation, Growth Drivers & Opportunities

According to Stellar Market Research, the Data Center Chip Market was valued at USD 10.84 billion in 2023 and is projected to grow at a CAGR of 8.1%, reaching USD 18.79 billion by 2030. The market's upward trajectory is fueled by the explosive rise in AI-driven applications, cloud computing, and the increasing demand for hyperscale data centers.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Data-Center-Chip-Market/2282

Key Growth Drivers:

AI & Machine Learning Expansion: Massive AI workloads in language models, computer vision, and predictive analytics are prompting demand for high-performance chips with superior throughput and power efficiency.

Cloud Service Growth: Public cloud giants such as AWS, Microsoft Azure, and Google Cloud continue expanding their infrastructure, relying on powerful data center chips to ensure scalable and efficient performance.

Edge Computing: The proliferation of edge devices necessitates data processing closer to the source, driving demand for specialized chips like ASICs and FPGAs with low latency.

Sustainability Focus: The shift towards green and energy-efficient data centers is pushing innovation in low-power chips that reduce the environmental footprint of computing.

Opportunities:

Chip customization for AI/ML workloads (AI accelerators).

Development of energy-efficient chips to comply with global carbon neutrality goals.

Growing demand for quantum computing processors and neuromorphic chips.

Partnerships between chipmakers and hyperscale providers for co-designed silicon.

U.S. Market Trends and Investment in 2024

In 2024, the U.S. data center chip market saw significant investment as AI exploded across industries. Intel and AMD intensified competition by launching next-gen chips optimized for generative AI. Google’s announcement of TPU v5 and NVIDIA’s unveiling of the Blackwell GPU architecture further raised the performance bar in U.S.-based hyperscale centers.

Additionally, the CHIPS and Science Act continued to incentivize local semiconductor manufacturing. Intel expanded its Ohio facility to support domestic demand for high-performance chips. These investments aim to reduce dependence on foreign chipmakers while positioning the U.S. as a leader in AI-ready data center infrastructure.

Market Segmentation: Leading Segment by Market Share

Based on the Stellar Market Research report, the GPU (Graphics Processing Unit) segment holds the largest share of the market. GPUs have become the cornerstone of modern data centers due to their unmatched parallel processing power, critical for accelerating AI and ML workloads, deep learning, and real-time analytics.

NVIDIA dominates this segment with its H100 and new B100 Blackwell chips, which are used extensively in training large language models and powering inference at scale. Their role in delivering maximum performance-per-watt has made GPUs the preferred choice in modern AI data centers.

Competitive Analysis: Top 5 Companies

NVIDIA Corporation

The market leader in GPU-based data center chips, NVIDIA continues to lead innovation with the Hopper and Blackwell architectures. In 2024, NVIDIA deepened its partnerships with Microsoft, Meta, and Oracle to supply AI chips, expanding its dominance in hyperscale environments.

Advanced Micro Devices (AMD)

AMD gained substantial ground with its MI300 series AI accelerators, offering performance parity with NVIDIA in specific workloads. The company also expanded its EPYC server CPU lineup, focusing on power efficiency and performance-per-dollar optimization.

Intel Corporation

Intel remained strong in the CPU segment with its Xeon Scalable processors, and is increasingly investing in Gaudi AI accelerators after acquiring Habana Labs. Intel’s $20 billion Ohio fab investment in 2024 reaffirmed its commitment to secure domestic chip supply for U.S.-based data centers.

Broadcom Inc.

Broadcom provides custom ASICs and network chips used in major cloud providers’ infrastructures. In 2024, the company introduced advanced Ethernet switching chips for AI data center fabrics, enabling faster, more energy-efficient interconnects between GPUs.

Marvell Technology Group

Marvell continued to grow in the DPUs (Data Processing Units) and custom silicon segments. Its 2024 innovations in AI-specific DPUs help offload non-compute tasks from CPUs and GPUs, improving overall system efficiency and throughput.

Regional Analysis

USA: The U.S. holds a dominant share of the global data center chip market, driven by leading cloud service providers, high AI adoption, and government initiatives such as the CHIPS Act. Continued innovation and fab expansion position the country for sustained leadership.

UK: While smaller in chip manufacturing, the UK is expanding data center capacity through investments in green computing. London-based facilities now demand energy-efficient chips, pushing interest in ARM-based processors and next-gen GPUs.

Germany: Germany supports semiconductor and data center development through the EU Chips Act. Companies like SAP and Deutsche Telekom have committed to expanding local cloud operations, increasing demand for data center chips that balance performance and sustainability.

France: France is promoting sovereign cloud infrastructure and digital independence. Public and private partnerships with cloud and chip firms have led to initiatives focused on AI research centers and edge data centers, increasing demand for specialized chips.

Japan: Japan’s government announced over $7 billion in funding for semiconductor R&D in 2024. Domestic companies like Renesas and Fujitsu are collaborating with global partners to produce chips optimized for compact data centers and AI systems.

China: Despite export restrictions, China is rapidly developing homegrown data center chips. Companies like Alibaba and Huawei’s HiSilicon are investing in AI-centric processors, though geopolitical pressures challenge global expansion.

Conclusion

The Data Center Chip Market is undergoing a transformative shift, fueled by unprecedented demand for high-performance computing, cloud scalability, and AI acceleration. With the rise of generative AI, real-time analytics, and green data centers, chipmakers are racing to deliver energy-efficient, specialized silicon that meets modern computational needs.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

+91 9607365656

[email protected]

0 Comments

0 Shares

383 Views