Marine Urea Market Size to Grow at a CAGR of 7.7 % in the Forecast Period of 2025-2032

Marine Urea Market – Navigating Towards Sustainable Shipping Practices

Market Overview & Forecast

The Marine Urea Market pertains to the production and utilization of urea solutions, specifically AUS 40 grade, employed in Selective Catalytic Reduction (SCR) systems aboard marine vessels. These systems are integral in reducing nitrogen oxide (NOₓ) emissions, thereby aiding compliance with stringent international maritime environmental regulations.

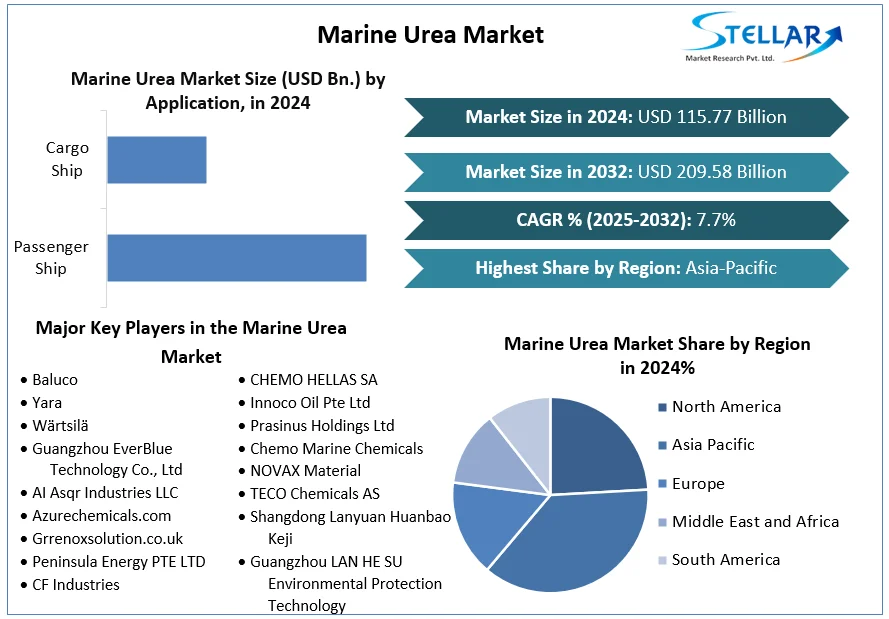

As of 2024, the global marine urea market was valued at approximately USD 115.77 billion. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.7% from 2025 to 2032, reaching an estimated USD 209.58 billion by 2032

Request Free Sample Report:

https://www.stellarmr.com/report/req_sample/marine-urea-market/2460

Market Drivers & Opportunities

Stringent Emission Regulations: International Maritime Organization (IMO) regulations, such as the IMO 2020 sulfur cap and NOₓ emission limits, are compelling shipping companies to adopt SCR systems, thereby driving the demand for marine urea.

Environmental Awareness: Growing global emphasis on reducing maritime pollution is fostering the adoption of cleaner technologies, including the use of marine urea in emission control systems.

Fleet Modernization: The ongoing trend of retrofitting existing vessels with SCR systems and the construction of new ships equipped with such technologies are contributing to the increased demand for marine urea.

Regional Initiatives: Countries with major shipping industries are implementing policies to promote the use of emission-reducing technologies, further propelling market growth.

Emerging Trends Shaping the Future

Integration with Alternative Fuels: The compatibility of marine urea with alternative fuels, such as LNG, is enhancing its appeal as part of comprehensive emission reduction strategies.

Advancements in SCR Technology: Continuous improvements in SCR systems are increasing their efficiency, thereby optimizing the consumption of marine urea and reducing operational costs.

Digitalization and Monitoring: The incorporation of digital technologies for real-time monitoring of NOₓ emissions and urea consumption is enabling better management and optimization of marine urea usage.

Sustainable Production Practices: Manufacturers are focusing on sustainable production methods for marine urea, aligning with the broader maritime industry's sustainability goals.

Segmentation Analysis

By Type:

AUS 40 Grade Marine Urea: The most commonly used grade, comprising 40% urea, is predominantly utilized in SCR systems for NOₓ reduction.

By Application:

Cargo Ships: The largest segment, driven by the high volume of global trade and the need for emission compliance.

Passenger Vessels: Includes cruise ships and ferries, where environmental regulations are stringent.

Naval and Military Ships: Adoption of SCR systems in defense vessels to meet emission standards.

By Region:

Asia-Pacific: The largest market share, attributed to the significant number of vessels operating in the region and stringent emission regulations.

Europe: Notable growth due to the implementation of strict environmental policies and the presence of major shipping hubs.

North America: Increasing adoption driven by regulatory requirements and environmental initiatives.

Competitive Landscape

Key players in the marine urea market include:

Yara International ASA: A leading global supplier of marine urea solutions, known for its commitment to sustainability and innovation.

CF Industries Holdings, Inc.: A major producer of urea products, including marine-grade urea solutions.

OCI N.V.: A global producer of nitrogen fertilizers and industrial chemicals, offering marine urea solutions.

SABIC: A diversified chemicals manufacturer providing marine urea products to the maritime industry.

EuroChem Group AG: A global fertilizer company supplying marine urea solutions to meet emission control requirements.

Competitive Strategies: Companies are focusing on product innovation, regulatory compliance, and strategic partnerships to strengthen their market position. Investments in research and development are leading to the creation of advanced marine urea solutions that meet evolving environmental standards.

Press Release Conclusion

The Marine Urea Market is experiencing significant growth, driven by stringent emission regulations, environmental awareness, and the modernization of the global shipping fleet. With a projected market size of USD 209.58 billion by 2032, the marine urea industry presents substantial opportunities for stakeholders across the value chain.

Companies that invest in innovation, sustainability practices, and regulatory compliance will be well-positioned to capitalize on the evolving market dynamics and contribute to the maritime industry's transition towards greener operations.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]Marine Urea Market Size to Grow at a CAGR of 7.7 % in the Forecast Period of 2025-2032

Marine Urea Market – Navigating Towards Sustainable Shipping Practices

Market Overview & Forecast

The Marine Urea Market pertains to the production and utilization of urea solutions, specifically AUS 40 grade, employed in Selective Catalytic Reduction (SCR) systems aboard marine vessels. These systems are integral in reducing nitrogen oxide (NOₓ) emissions, thereby aiding compliance with stringent international maritime environmental regulations.

As of 2024, the global marine urea market was valued at approximately USD 115.77 billion. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.7% from 2025 to 2032, reaching an estimated USD 209.58 billion by 2032

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/marine-urea-market/2460

Market Drivers & Opportunities

Stringent Emission Regulations: International Maritime Organization (IMO) regulations, such as the IMO 2020 sulfur cap and NOₓ emission limits, are compelling shipping companies to adopt SCR systems, thereby driving the demand for marine urea.

Environmental Awareness: Growing global emphasis on reducing maritime pollution is fostering the adoption of cleaner technologies, including the use of marine urea in emission control systems.

Fleet Modernization: The ongoing trend of retrofitting existing vessels with SCR systems and the construction of new ships equipped with such technologies are contributing to the increased demand for marine urea.

Regional Initiatives: Countries with major shipping industries are implementing policies to promote the use of emission-reducing technologies, further propelling market growth.

Emerging Trends Shaping the Future

Integration with Alternative Fuels: The compatibility of marine urea with alternative fuels, such as LNG, is enhancing its appeal as part of comprehensive emission reduction strategies.

Advancements in SCR Technology: Continuous improvements in SCR systems are increasing their efficiency, thereby optimizing the consumption of marine urea and reducing operational costs.

Digitalization and Monitoring: The incorporation of digital technologies for real-time monitoring of NOₓ emissions and urea consumption is enabling better management and optimization of marine urea usage.

Sustainable Production Practices: Manufacturers are focusing on sustainable production methods for marine urea, aligning with the broader maritime industry's sustainability goals.

Segmentation Analysis

By Type:

AUS 40 Grade Marine Urea: The most commonly used grade, comprising 40% urea, is predominantly utilized in SCR systems for NOₓ reduction.

By Application:

Cargo Ships: The largest segment, driven by the high volume of global trade and the need for emission compliance.

Passenger Vessels: Includes cruise ships and ferries, where environmental regulations are stringent.

Naval and Military Ships: Adoption of SCR systems in defense vessels to meet emission standards.

By Region:

Asia-Pacific: The largest market share, attributed to the significant number of vessels operating in the region and stringent emission regulations.

Europe: Notable growth due to the implementation of strict environmental policies and the presence of major shipping hubs.

North America: Increasing adoption driven by regulatory requirements and environmental initiatives.

Competitive Landscape

Key players in the marine urea market include:

Yara International ASA: A leading global supplier of marine urea solutions, known for its commitment to sustainability and innovation.

CF Industries Holdings, Inc.: A major producer of urea products, including marine-grade urea solutions.

OCI N.V.: A global producer of nitrogen fertilizers and industrial chemicals, offering marine urea solutions.

SABIC: A diversified chemicals manufacturer providing marine urea products to the maritime industry.

EuroChem Group AG: A global fertilizer company supplying marine urea solutions to meet emission control requirements.

Competitive Strategies: Companies are focusing on product innovation, regulatory compliance, and strategic partnerships to strengthen their market position. Investments in research and development are leading to the creation of advanced marine urea solutions that meet evolving environmental standards.

Press Release Conclusion

The Marine Urea Market is experiencing significant growth, driven by stringent emission regulations, environmental awareness, and the modernization of the global shipping fleet. With a projected market size of USD 209.58 billion by 2032, the marine urea industry presents substantial opportunities for stakeholders across the value chain.

Companies that invest in innovation, sustainability practices, and regulatory compliance will be well-positioned to capitalize on the evolving market dynamics and contribute to the maritime industry's transition towards greener operations.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]