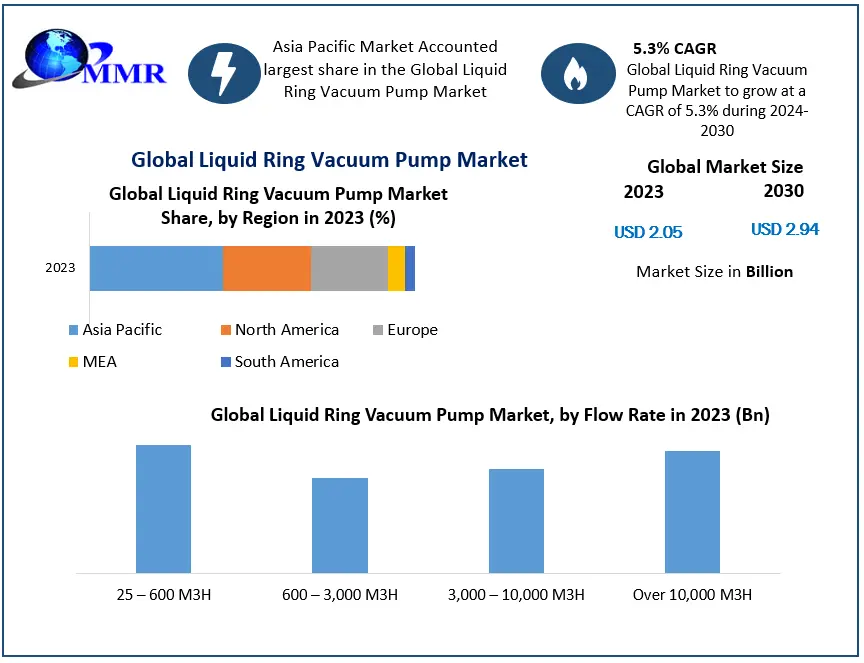

Liquid Ring Vacuum Pump Market Size To Grow At A CAGR Of 5.3% In The Forecast Period Of 2024-2030

Liquid Ring Vacuum Pump Market is poised for significant growth, with projections indicating an expansion from USD 2.05 billion in 2023 to USD 2.94 billion by 2030. This growth is driven by increasing demand across industries such as oil & gas, chemical processing, and power generation, coupled with the pumps' energy-efficient and reliable performance.

Request Free Sample Report:

https://www.maximizemarketresearch.com/request-sample/221378/

Market Estimation & Definition

Liquid ring vacuum pumps are positive displacement pumps that utilize a rotating mechanism to compress gas and create a vacuum. They are particularly effective in handling wet or saturated gases, making them suitable for applications where the pumped media contains liquids. Their robust construction and ability to operate in demanding conditions contribute to their widespread adoption in various industrial settings.

Market Growth Drivers & Opportunities

Several factors are propelling the growth of the liquid ring vacuum pump market:

Industrial Demand: Industries such as oil & gas, chemical processing, and power generation rely on liquid ring vacuum pumps for applications like gas compression, vacuum generation, and degassing processes.

Energy Efficiency: These pumps operate with high efficiency due to the use of water as a sealing and cooling medium, reducing the need for extra lubrication and minimizing energy loss.

Reliability and Low Maintenance: The simple design with fewer moving parts leads to lower maintenance requirements, making them a cost-effective choice for various manufacturing processes.

Segmentation Analysis

The liquid ring vacuum pump market is segmented based on flow rate, stage, material, and end-user industries:

By Flow Rate:

25–600 M³/H

600–3,000 M³/H

3,000–10,000 M³/H

Over 10,000 M³/H

By Stage:

Single-Stage

Multiple-Stage

By Material:

Stainless Steel

Cast Iron

Others

By End-User Industry:

Oil & Gas

Chemical Processing

Power Generation

Pharmaceuticals

Food & Beverage

Pulp & Paper

Water Treatment

Others

Country-Level Analysis: USA and Germany

United States: The U.S. market is experiencing growth due to advanced industrial infrastructure and a strong focus on technological innovation. The adoption of liquid ring vacuum pumps is significant in sectors like oil & gas, pharmaceuticals, and food processing.

Germany: Germany's emphasis on sustainable and energy-efficient solutions drives the demand for liquid ring vacuum pumps. The country's robust manufacturing sector and adherence to strict environmental regulations contribute to market growth.

Competitive Analysis

The liquid ring vacuum pump market is characterized by the presence of several key players focusing on innovation and strategic partnerships:

Atlas Copco: Offers a range of vacuum solutions with a focus on energy efficiency and sustainability.

Flowserve Corporation: Provides comprehensive flow control solutions, including liquid ring vacuum pumps for various industries.

Busch Vacuum Solutions: Specializes in vacuum and overpressure technology, offering reliable liquid ring vacuum pumps.

Cutes Corp.: Known for technological advancements in fluid motion and vacuum technology.

Graham Corporation: Offers engineered vacuum and heat transfer equipment for process industries.

Conclusion

The global liquid ring vacuum pump market is set for robust growth, driven by increasing industrial demand, energy efficiency, and reliability. As industries continue to seek sustainable and cost-effective solutions, the adoption of liquid ring vacuum pumps is expected to rise, presenting opportunities for innovation and market expansion.

Related report:

Cybersecurity mesh market:

https://www.maximizemarketresearch.com/market-report/cybersecurity-mesh-market/200224/

Application performance monitoring market:

https://www.maximizemarketresearch.com/market-report/application-performance-monitoring-market/200134/

About Us

Maximize Market Research is one of the fastest-growing market research and business consulting firms serving clients globally. Our revenue impact and focused growth-driven research initiatives make us a proud partner of majority of the Fortune 500 companies. We have a diversified portfolio and serve a variety of industries such as IT & telecom, chemical, food & beverage, aerospace & defense, healthcare and others.

MAXIMIZE MARKET RESEARCH PVT. LTD.

2nd Floor, Navale IT park Phase 3,

Pune Banglore Highway, Narhe

Pune, Maharashtra 411041, India.

+91 9607365656

[email protected]Liquid Ring Vacuum Pump Market Size To Grow At A CAGR Of 5.3% In The Forecast Period Of 2024-2030

Liquid Ring Vacuum Pump Market is poised for significant growth, with projections indicating an expansion from USD 2.05 billion in 2023 to USD 2.94 billion by 2030. This growth is driven by increasing demand across industries such as oil & gas, chemical processing, and power generation, coupled with the pumps' energy-efficient and reliable performance.

Request Free Sample Report:https://www.maximizemarketresearch.com/request-sample/221378/

Market Estimation & Definition

Liquid ring vacuum pumps are positive displacement pumps that utilize a rotating mechanism to compress gas and create a vacuum. They are particularly effective in handling wet or saturated gases, making them suitable for applications where the pumped media contains liquids. Their robust construction and ability to operate in demanding conditions contribute to their widespread adoption in various industrial settings.

Market Growth Drivers & Opportunities

Several factors are propelling the growth of the liquid ring vacuum pump market:

Industrial Demand: Industries such as oil & gas, chemical processing, and power generation rely on liquid ring vacuum pumps for applications like gas compression, vacuum generation, and degassing processes.

Energy Efficiency: These pumps operate with high efficiency due to the use of water as a sealing and cooling medium, reducing the need for extra lubrication and minimizing energy loss.

Reliability and Low Maintenance: The simple design with fewer moving parts leads to lower maintenance requirements, making them a cost-effective choice for various manufacturing processes.

Segmentation Analysis

The liquid ring vacuum pump market is segmented based on flow rate, stage, material, and end-user industries:

By Flow Rate:

25–600 M³/H

600–3,000 M³/H

3,000–10,000 M³/H

Over 10,000 M³/H

By Stage:

Single-Stage

Multiple-Stage

By Material:

Stainless Steel

Cast Iron

Others

By End-User Industry:

Oil & Gas

Chemical Processing

Power Generation

Pharmaceuticals

Food & Beverage

Pulp & Paper

Water Treatment

Others

Country-Level Analysis: USA and Germany

United States: The U.S. market is experiencing growth due to advanced industrial infrastructure and a strong focus on technological innovation. The adoption of liquid ring vacuum pumps is significant in sectors like oil & gas, pharmaceuticals, and food processing.

Germany: Germany's emphasis on sustainable and energy-efficient solutions drives the demand for liquid ring vacuum pumps. The country's robust manufacturing sector and adherence to strict environmental regulations contribute to market growth.

Competitive Analysis

The liquid ring vacuum pump market is characterized by the presence of several key players focusing on innovation and strategic partnerships:

Atlas Copco: Offers a range of vacuum solutions with a focus on energy efficiency and sustainability.

Flowserve Corporation: Provides comprehensive flow control solutions, including liquid ring vacuum pumps for various industries.

Busch Vacuum Solutions: Specializes in vacuum and overpressure technology, offering reliable liquid ring vacuum pumps.

Cutes Corp.: Known for technological advancements in fluid motion and vacuum technology.

Graham Corporation: Offers engineered vacuum and heat transfer equipment for process industries.

Conclusion

The global liquid ring vacuum pump market is set for robust growth, driven by increasing industrial demand, energy efficiency, and reliability. As industries continue to seek sustainable and cost-effective solutions, the adoption of liquid ring vacuum pumps is expected to rise, presenting opportunities for innovation and market expansion.

Related report:

Cybersecurity mesh market:

https://www.maximizemarketresearch.com/market-report/cybersecurity-mesh-market/200224/

Application performance monitoring market:

https://www.maximizemarketresearch.com/market-report/application-performance-monitoring-market/200134/

About Us

Maximize Market Research is one of the fastest-growing market research and business consulting firms serving clients globally. Our revenue impact and focused growth-driven research initiatives make us a proud partner of majority of the Fortune 500 companies. We have a diversified portfolio and serve a variety of industries such as IT & telecom, chemical, food & beverage, aerospace & defense, healthcare and others.

MAXIMIZE MARKET RESEARCH PVT. LTD.

2nd Floor, Navale IT park Phase 3,

Pune Banglore Highway, Narhe

Pune, Maharashtra 411041, India.

+91 9607365656

[email protected]