North America Organic Food Market Size to Grow at a CAGR of 13.50% in the Forecast Period of 2025-2032

North America Organic Food Market – Growth, Trends, and Future Outlook

1. Market Estimation & Definition

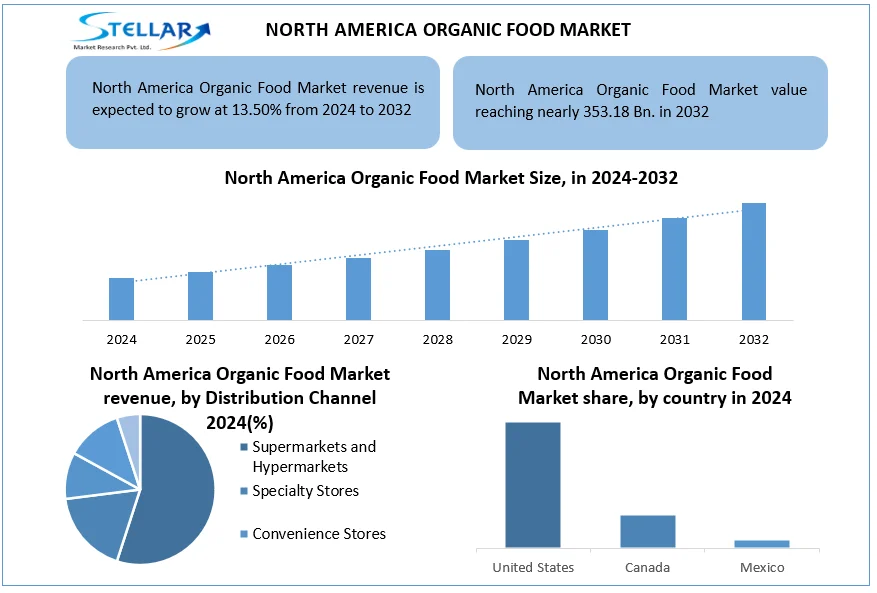

The North American organic food market was valued at approximately USD 128.24 billion in 2024 and is projected to reach around USD 353.18 billion by 2032, growing at a compound annual growth rate (CAGR) of 13.50% during the forecast period . This market encompasses all food products produced without synthetic pesticides, genetically modified organisms (GMOs), or artificial additives, emphasizing natural farming practices and sustainability.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/north-america-organic-food-market/2721

2. Market Growth Drivers & Opportunities

Several factors are fueling the growth of the organic food market in North America:

Health Consciousness: Consumers are increasingly aware of the health risks associated with conventional farming practices, leading to a higher demand for organic products.

Sustainability Concerns: Growing environmental awareness is prompting consumers to choose products that are produced using eco-friendly methods.

Government Support: Policies and subsidies supporting organic farming practices are encouraging more producers to transition to organic methods.

Technological Advancements: Innovations in farming techniques and supply chain management are making organic food production more efficient and accessible.

3. What Lies Ahead: Emerging Trends Shaping the Future

The future of the organic food market in North America is being shaped by several emerging trends:

Plant-Based Diets: An increasing number of consumers are adopting plant-based diets, driving the demand for organic plant-based food products.

Clean Label Products: There is a growing preference for products with minimal and transparent ingredient lists, leading to a rise in clean label organic foods.

E-commerce Growth: Online platforms are becoming significant channels for organic food sales, providing consumers with greater access to a variety of organic products.

Local Sourcing: Consumers are showing a preference for locally sourced organic products, supporting regional economies and reducing carbon footprints.

4. Segmentation Analysis

The North American organic food market can be segmented based on product type, distribution channel, and country:

By Product Type:

Fruits & Vegetables: These remain the largest segment, accounting for a significant share of the market.

Dairy Products: Organic dairy products are gaining popularity due to perceived health benefits.

Meat & Poultry: There is a growing demand for organic meat and poultry products.

Packaged Foods: Organic packaged foods are expanding as consumers seek convenient yet healthy options.

By Distribution Channel:

Offline: Traditional retail stores continue to be the dominant channel for organic food sales.

Online: E-commerce platforms are witnessing significant growth, offering consumers convenience and a wider range of products.

By Country:

United States: The U.S. holds the largest share of the North American organic food market, driven by high consumer demand and a well-established organic farming sector.

Canada: Canada's organic food market is expanding, supported by increasing consumer awareness and government initiatives promoting organic agriculture.

Mexico: Mexico is emerging as a significant player in the organic food market, with growing domestic production and export opportunities.

5. Country-Level Analysis

United States: The U.S. organic food market is the largest in North America, with sales reaching USD 71.6 billion in 2024, marking a 5.2% increase from the previous year . The market is characterized by a diverse range of organic products and a robust distribution network.

Canada: Canada's organic food market is experiencing steady growth, driven by consumer demand for healthier and more sustainable food options. Government policies supporting organic farming practices are also contributing to market expansion.

Mexico: Mexico is increasingly becoming a significant exporter of organic food products, particularly fruits and vegetables, to international markets. Domestic consumption is also rising as consumers become more health-conscious.

6. Competitive Landscape

The North American organic food market is competitive, with several key players:

General Mills: Offers a range of organic products under brands like Annie's and Cascadian Farm.

Nestlé: Provides organic food options through its various brands, catering to the growing demand for organic products.

Danone: Offers organic dairy and plant-based products, focusing on health and sustainability.

Whole Foods Market: A leading retailer specializing in organic and natural foods, with a strong presence in the U.S.

Costco: Offers a wide range of organic products at competitive prices, attracting a broad consumer base.

7. Press Release Conclusion

The North American organic food market is poised for significant growth, driven by increasing consumer awareness of health and environmental issues, supportive government policies, and advancements in organic farming practices. As consumers continue to seek healthier and more sustainable food options, the demand for organic products is expected to rise, presenting opportunities for producers, retailers, and investors in the organic food sector.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

North America Organic Food Market – Growth, Trends, and Future Outlook

1. Market Estimation & Definition

The North American organic food market was valued at approximately USD 128.24 billion in 2024 and is projected to reach around USD 353.18 billion by 2032, growing at a compound annual growth rate (CAGR) of 13.50% during the forecast period . This market encompasses all food products produced without synthetic pesticides, genetically modified organisms (GMOs), or artificial additives, emphasizing natural farming practices and sustainability.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/north-america-organic-food-market/2721

2. Market Growth Drivers & Opportunities

Several factors are fueling the growth of the organic food market in North America:

Health Consciousness: Consumers are increasingly aware of the health risks associated with conventional farming practices, leading to a higher demand for organic products.

Sustainability Concerns: Growing environmental awareness is prompting consumers to choose products that are produced using eco-friendly methods.

Government Support: Policies and subsidies supporting organic farming practices are encouraging more producers to transition to organic methods.

Technological Advancements: Innovations in farming techniques and supply chain management are making organic food production more efficient and accessible.

3. What Lies Ahead: Emerging Trends Shaping the Future

The future of the organic food market in North America is being shaped by several emerging trends:

Plant-Based Diets: An increasing number of consumers are adopting plant-based diets, driving the demand for organic plant-based food products.

Clean Label Products: There is a growing preference for products with minimal and transparent ingredient lists, leading to a rise in clean label organic foods.

E-commerce Growth: Online platforms are becoming significant channels for organic food sales, providing consumers with greater access to a variety of organic products.

Local Sourcing: Consumers are showing a preference for locally sourced organic products, supporting regional economies and reducing carbon footprints.

4. Segmentation Analysis

The North American organic food market can be segmented based on product type, distribution channel, and country:

By Product Type:

Fruits & Vegetables: These remain the largest segment, accounting for a significant share of the market.

Dairy Products: Organic dairy products are gaining popularity due to perceived health benefits.

Meat & Poultry: There is a growing demand for organic meat and poultry products.

Packaged Foods: Organic packaged foods are expanding as consumers seek convenient yet healthy options.

By Distribution Channel:

Offline: Traditional retail stores continue to be the dominant channel for organic food sales.

Online: E-commerce platforms are witnessing significant growth, offering consumers convenience and a wider range of products.

By Country:

United States: The U.S. holds the largest share of the North American organic food market, driven by high consumer demand and a well-established organic farming sector.

Canada: Canada's organic food market is expanding, supported by increasing consumer awareness and government initiatives promoting organic agriculture.

Mexico: Mexico is emerging as a significant player in the organic food market, with growing domestic production and export opportunities.

5. Country-Level Analysis

United States: The U.S. organic food market is the largest in North America, with sales reaching USD 71.6 billion in 2024, marking a 5.2% increase from the previous year . The market is characterized by a diverse range of organic products and a robust distribution network.

Canada: Canada's organic food market is experiencing steady growth, driven by consumer demand for healthier and more sustainable food options. Government policies supporting organic farming practices are also contributing to market expansion.

Mexico: Mexico is increasingly becoming a significant exporter of organic food products, particularly fruits and vegetables, to international markets. Domestic consumption is also rising as consumers become more health-conscious.

6. Competitive Landscape

The North American organic food market is competitive, with several key players:

General Mills: Offers a range of organic products under brands like Annie's and Cascadian Farm.

Nestlé: Provides organic food options through its various brands, catering to the growing demand for organic products.

Danone: Offers organic dairy and plant-based products, focusing on health and sustainability.

Whole Foods Market: A leading retailer specializing in organic and natural foods, with a strong presence in the U.S.

Costco: Offers a wide range of organic products at competitive prices, attracting a broad consumer base.

7. Press Release Conclusion

The North American organic food market is poised for significant growth, driven by increasing consumer awareness of health and environmental issues, supportive government policies, and advancements in organic farming practices. As consumers continue to seek healthier and more sustainable food options, the demand for organic products is expected to rise, presenting opportunities for producers, retailers, and investors in the organic food sector.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

North America Organic Food Market Size to Grow at a CAGR of 13.50% in the Forecast Period of 2025-2032

North America Organic Food Market – Growth, Trends, and Future Outlook

1. Market Estimation & Definition

The North American organic food market was valued at approximately USD 128.24 billion in 2024 and is projected to reach around USD 353.18 billion by 2032, growing at a compound annual growth rate (CAGR) of 13.50% during the forecast period . This market encompasses all food products produced without synthetic pesticides, genetically modified organisms (GMOs), or artificial additives, emphasizing natural farming practices and sustainability.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/north-america-organic-food-market/2721

2. Market Growth Drivers & Opportunities

Several factors are fueling the growth of the organic food market in North America:

Health Consciousness: Consumers are increasingly aware of the health risks associated with conventional farming practices, leading to a higher demand for organic products.

Sustainability Concerns: Growing environmental awareness is prompting consumers to choose products that are produced using eco-friendly methods.

Government Support: Policies and subsidies supporting organic farming practices are encouraging more producers to transition to organic methods.

Technological Advancements: Innovations in farming techniques and supply chain management are making organic food production more efficient and accessible.

3. What Lies Ahead: Emerging Trends Shaping the Future

The future of the organic food market in North America is being shaped by several emerging trends:

Plant-Based Diets: An increasing number of consumers are adopting plant-based diets, driving the demand for organic plant-based food products.

Clean Label Products: There is a growing preference for products with minimal and transparent ingredient lists, leading to a rise in clean label organic foods.

E-commerce Growth: Online platforms are becoming significant channels for organic food sales, providing consumers with greater access to a variety of organic products.

Local Sourcing: Consumers are showing a preference for locally sourced organic products, supporting regional economies and reducing carbon footprints.

4. Segmentation Analysis

The North American organic food market can be segmented based on product type, distribution channel, and country:

By Product Type:

Fruits & Vegetables: These remain the largest segment, accounting for a significant share of the market.

Dairy Products: Organic dairy products are gaining popularity due to perceived health benefits.

Meat & Poultry: There is a growing demand for organic meat and poultry products.

Packaged Foods: Organic packaged foods are expanding as consumers seek convenient yet healthy options.

By Distribution Channel:

Offline: Traditional retail stores continue to be the dominant channel for organic food sales.

Online: E-commerce platforms are witnessing significant growth, offering consumers convenience and a wider range of products.

By Country:

United States: The U.S. holds the largest share of the North American organic food market, driven by high consumer demand and a well-established organic farming sector.

Canada: Canada's organic food market is expanding, supported by increasing consumer awareness and government initiatives promoting organic agriculture.

Mexico: Mexico is emerging as a significant player in the organic food market, with growing domestic production and export opportunities.

5. Country-Level Analysis

United States: The U.S. organic food market is the largest in North America, with sales reaching USD 71.6 billion in 2024, marking a 5.2% increase from the previous year . The market is characterized by a diverse range of organic products and a robust distribution network.

Canada: Canada's organic food market is experiencing steady growth, driven by consumer demand for healthier and more sustainable food options. Government policies supporting organic farming practices are also contributing to market expansion.

Mexico: Mexico is increasingly becoming a significant exporter of organic food products, particularly fruits and vegetables, to international markets. Domestic consumption is also rising as consumers become more health-conscious.

6. Competitive Landscape

The North American organic food market is competitive, with several key players:

General Mills: Offers a range of organic products under brands like Annie's and Cascadian Farm.

Nestlé: Provides organic food options through its various brands, catering to the growing demand for organic products.

Danone: Offers organic dairy and plant-based products, focusing on health and sustainability.

Whole Foods Market: A leading retailer specializing in organic and natural foods, with a strong presence in the U.S.

Costco: Offers a wide range of organic products at competitive prices, attracting a broad consumer base.

7. Press Release Conclusion

The North American organic food market is poised for significant growth, driven by increasing consumer awareness of health and environmental issues, supportive government policies, and advancements in organic farming practices. As consumers continue to seek healthier and more sustainable food options, the demand for organic products is expected to rise, presenting opportunities for producers, retailers, and investors in the organic food sector.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

[email protected]

0 Bình luận

0 Chia sẻ

2268 Lượt xem